What Is Negative Gearing on a Property? How It Works

If you’re weighing up an investment property purchase, you’ve probably heard someone at a barbecue mention that negative gearing saves them a fortune on tax. It’s one of the most talked-about, and most misunderstood, strategies in Australian property investing, and getting the detail wrong can cost you thousands come tax time.

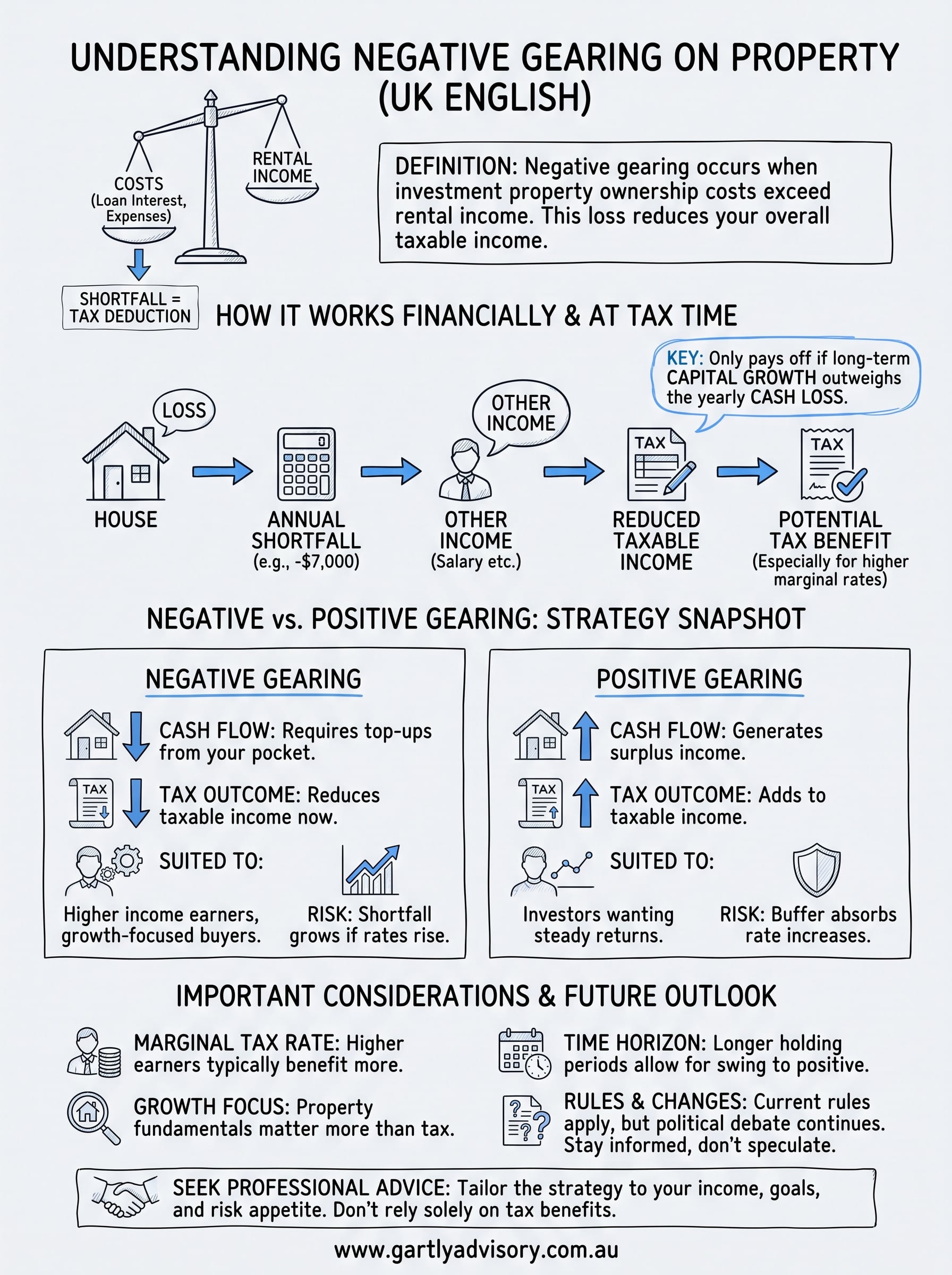

In simple terms, negative gearing happens when the costs of owning an investment property, including loan interest and running expenses, exceed the rental income it earns. That shortfall becomes a tax deduction against your other income, which is exactly why so many investors structure their portfolios this way. But it only makes sense in certain circumstances, and it’s not automatically the smartest move for every investor.

In this article, we’ll walk through exactly how negative gearing works financially and at tax time, weigh it against positive gearing, and cover the real benefits and drawbacks so you can judge whether it fits your own investment strategy.

Why negative gearing matters for property investors

Understanding what is negative gearing property ownership really means matters because it shapes almost every decision you make about buying, holding, and eventually selling an investment. Plenty of investors chase the tax deduction without checking whether the underlying property actually stacks up as a solid asset. That’s backwards. The tax benefit should be the icing, not the cake.

The appeal of an immediate tax offset

Gartly clients often come to us assuming negative gearing is a shortcut to wealth, when really it’s a cash flow tool that works best alongside genuine capital growth. When your rental property runs at a loss, that loss reduces your taxable income, which can mean a smaller tax bill or a bigger refund each year. For someone on a high marginal tax rate, this can materially soften the cost of holding an investment property while you wait for it to grow in value. The Australian Taxation Office confirms this deduction is legitimate under current tax law, provided the property is genuinely available for rent and the expenses are properly substantiated, as outlined on the ATO’s rental properties guidance.

Negative gearing only pays off when the property’s long-term growth outweighs the yearly cash you’re losing to fund it.

Why it matters beyond tax time

Negative gearing matters because it directly affects your cash flow planning, your borrowing capacity for future purchases, and how resilient your portfolio is if interest rates rise or a tenant moves out. A property that’s negatively geared today might turn positively geared in five or ten years as rents climb and the loan balance shrinks, so the strategy is really about timing and patience, not a permanent tax loophole.

Here’s a quick snapshot of what typically drives investors towards this approach:

- Marginal tax rate: higher earners get more benefit from the deduction

- Growth expectations: strong capital growth areas justify short-term losses

- Loan structure: interest-only periods often increase the negative gearing effect

- Holding period: longer timeframes give the property more chance to swing positive

Factoring in these elements before you buy, rather than after settlement, saves a lot of regret later on.

How negative gearing works in practice

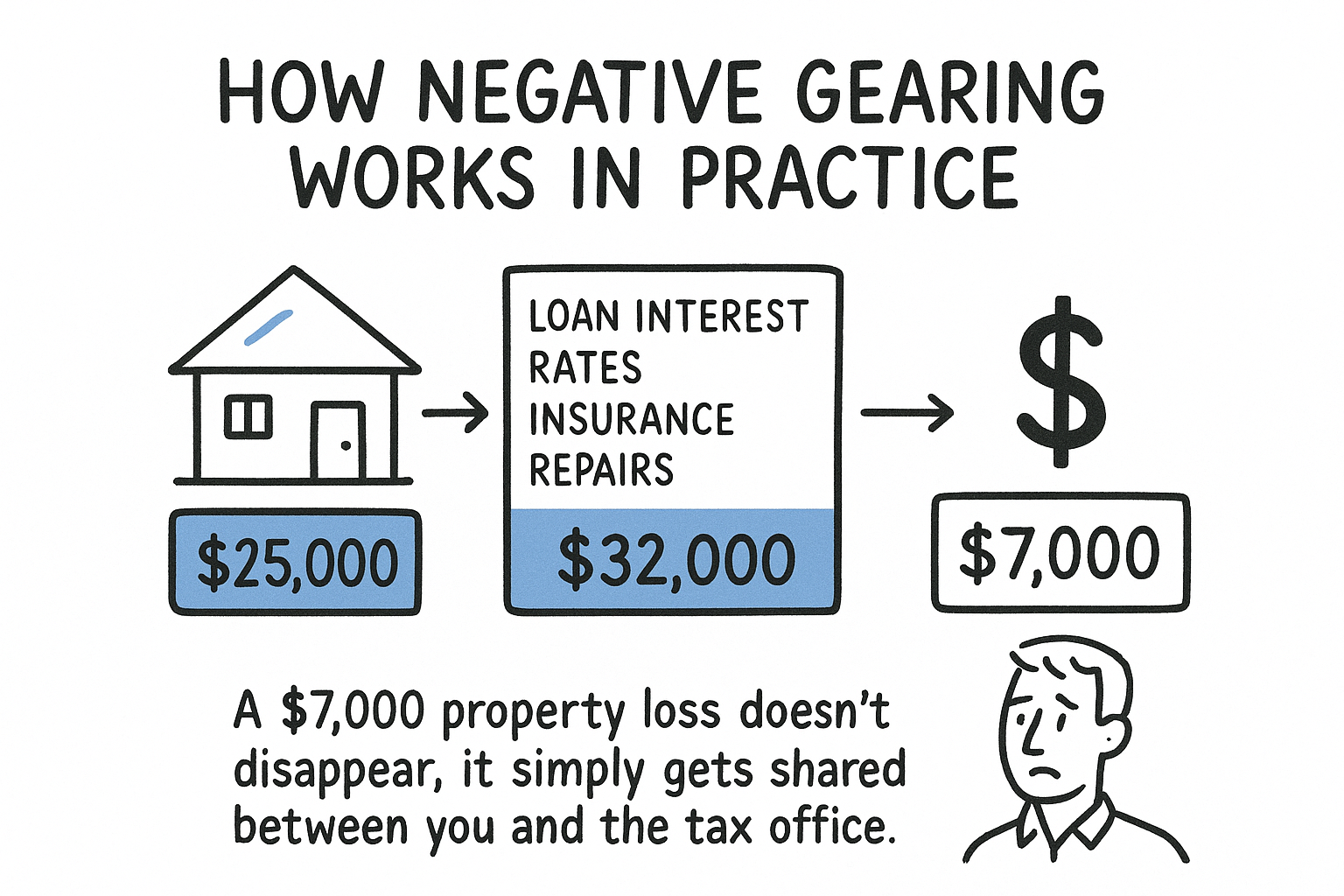

Running the numbers is the only way to see whether negative gearing actually stacks up for your situation, so let’s walk through a realistic example. Say you own an investment property earning $25,000 a year in rent, but your loan interest, council rates, insurance, property management fees, and repairs add up to $32,000. That leaves a $7,000 shortfall, which becomes your negative gearing deduction against your other taxable income for the year.

A worked example

Take a table to see how that shortfall flows through to your tax outcome:

| Item | Amount |

|---|---|

| Rental income | $25,000 |

| Loan interest, rates, insurance, repairs, management fees | $32,000 |

| Net rental loss | $7,000 |

| Marginal tax rate | 37% |

| Tax saving from deduction | $2,590 |

A $7,000 property loss doesn’t disappear, it simply gets shared between you and the tax office.

Where the deduction actually applies

Once you’ve calculated the loss, it gets added to your other assessable income, such as your salary, and reduces the total amount you’re taxed on. So instead of paying tax on your full wage, you’re taxed on your wage minus that $7,000 loss. Depreciation on fixtures and the building itself can widen this gap further, even though it’s not an out-of-pocket cost, which is why getting a quantity surveyor’s depreciation schedule done early is worth the fee.

Getting this calculation right depends heavily on accurate expense tracking throughout the year, not just at tax time, because the Australian Taxation Office expects every claimed deduction to be properly substantiated with receipts and records.

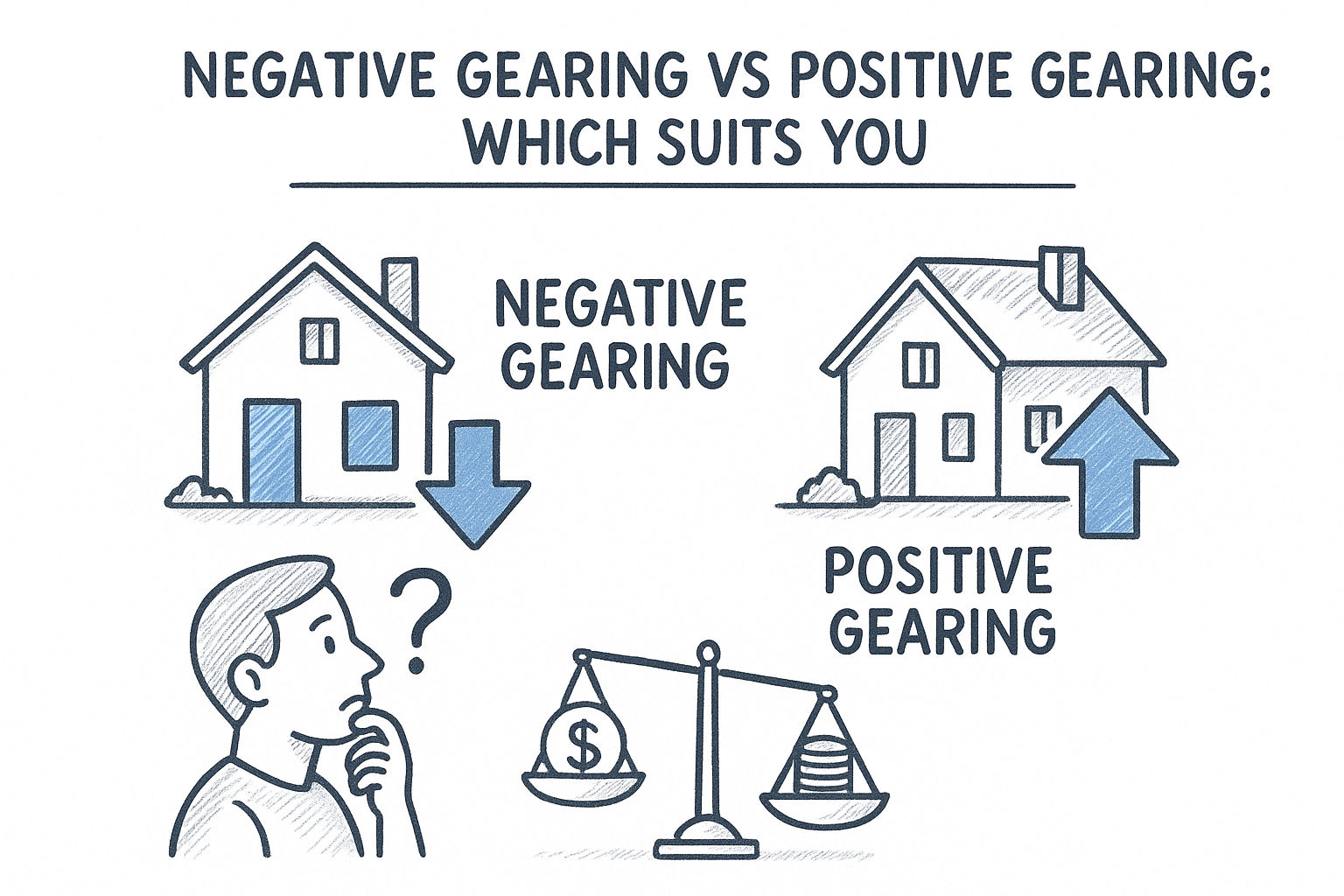

Negative gearing vs positive gearing: which suits you

Choosing between negative gearing and positive gearing isn’t a one-size-fits-all decision, it depends on your income, your appetite for risk, and how long you’re prepared to hold the asset. Negative gearing suits investors who earn a solid income now, expect strong capital growth, and can comfortably absorb a yearly shortfall while waiting for the property to climb in value. Positive gearing, where rental income exceeds expenses, suits investors who want immediate cash flow and less reliance on tax time to make the numbers work.

Weighing the two side by side

A quick comparison makes the trade-offs obvious:

| Factor | Negative gearing | Positive gearing |

|---|---|---|

| Cash flow | Requires top-ups from your own pocket | Generates surplus income |

| Tax outcome | Reduces taxable income now | Adds to taxable income |

| Best suited to | Higher income earners, growth-focused buyers | Investors wanting steady returns |

| Risk if rates rise | Shortfall grows | Buffer absorbs increases |

The right choice comes down to whether you need income today or growth tomorrow.

Matching the strategy to your goals

Someone nearing retirement, for example, usually leans towards positive gearing because they need reliable income rather than a tax deduction that only pays off years down the track. Younger investors with strong salaries often prefer negative gearing because the deduction eases cash flow pressure while their borrowing capacity and career earnings are still climbing. Ultimately, the smartest approach blends both across a portfolio, so you’re not entirely dependent on tax refunds or entirely exposed to vacancy risk. Talking through your income trajectory and long-term goals with an adviser before you commit to either path avoids locking yourself into a structure that no longer suits you in five years.

Upcoming changes to negative gearing rules

Negative gearing has been a political football in Australia for decades, and the debate hasn’t gone away. Various governments and think tanks have floated capping the deduction, grandfathering existing investors, or scrapping it altogether for new purchases, but nothing has been legislated to change how the rules apply right now. If you’re planning a purchase, it pays to know the difference between genuine policy and election-season noise.

Where the debate currently stands

Treasury has periodically modelled the revenue and housing affordability effects of negative gearing, and these reports resurface every time housing prices climb. The Australian Taxation Office continues to apply the existing deduction rules exactly as they stand today, and any reform would almost certainly require legislation passed through Parliament, not just a policy announcement. You can track official positions through the Treasury’s housing policy updates rather than relying on headlines.

Until Parliament actually changes the law, the current negative gearing rules still apply in full.

What investors should keep an eye on

Rather than guessing at future changes, focus on what’s within your control:

- Grandfathering clauses: past reform proposals have protected existing investments, so timing your purchase matters less than getting the fundamentals right

- State-based land tax changes: these move faster than federal negative gearing rules and affect your holding costs sooner

- Loan serviceability buffers: lenders adjust these regardless of tax policy, and they affect your borrowing capacity

Staying informed beats reacting to speculation, and reviewing your structure annually with your accountant keeps you ready for whatever change eventually lands.

Getting the right advice for your situation

Negative gearing can be a genuinely useful tool, but only when it’s built around a property that stacks up on its own merits, not just its tax deduction. You’ve seen how the numbers flow through, how it compares against positive gearing, and why the current rules could shift with the political wind. What works for your neighbour’s portfolio or your mate’s rental might not suit your income, your timeline, or your appetite for risk.

Running these numbers properly, factoring in depreciation, loan structure, and your own marginal tax rate, takes more than a quick online calculator. It takes someone who understands both the tax law and the commercial reality of holding property long term. That’s where a second set of eyes pays for itself many times over.

If you’re weighing up an investment property or reviewing an existing portfolio, talk to the team at Gartly Advisory about whether negative gearing genuinely fits your strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}