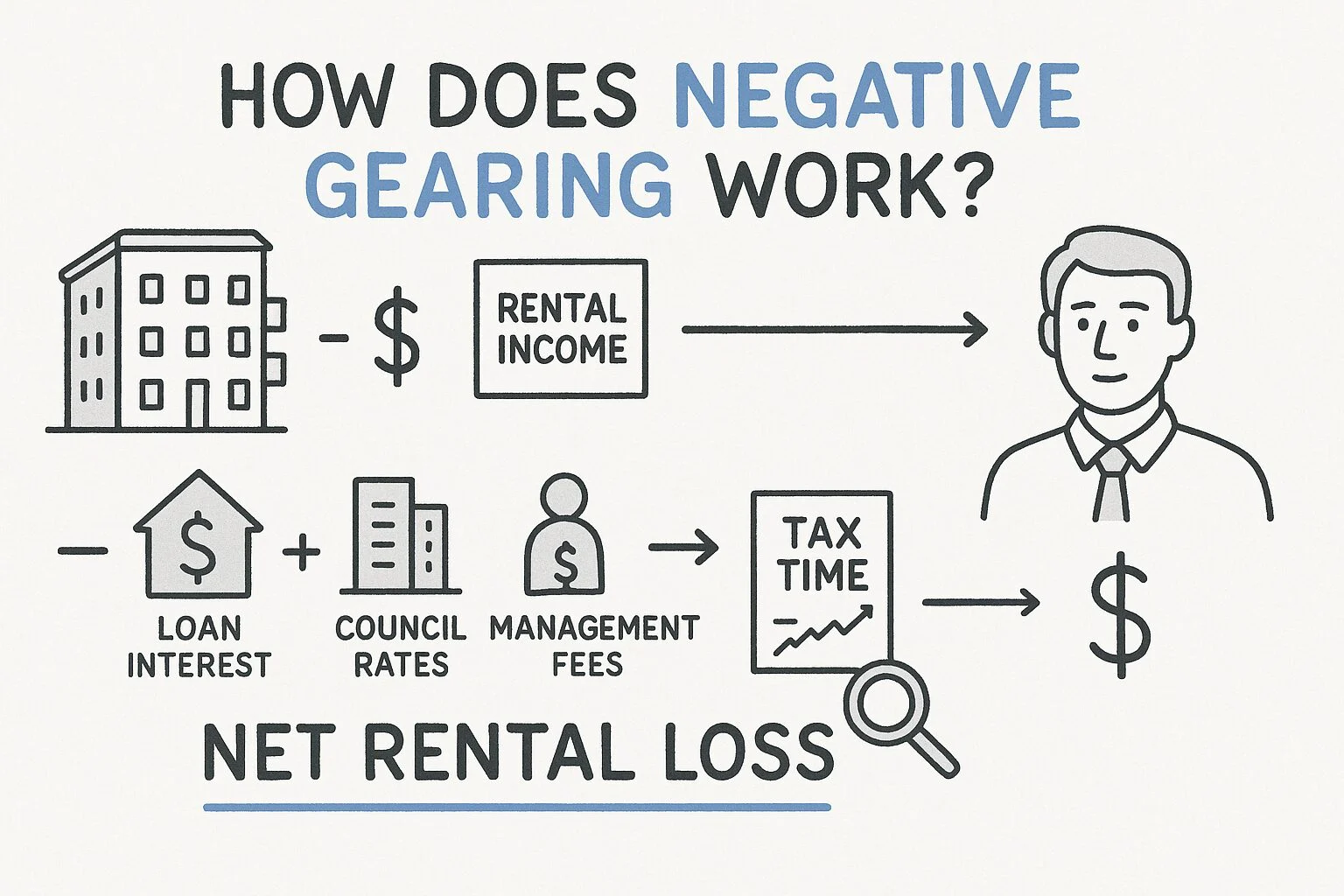

How Does Negative Gearing Work? A Step-by-Step Breakdown

If you own an investment property that costs you more to hold than it earns in rent, you have probably heard the term thrown around at a barbecue without ever getting a proper explanation. How does negative gearing work in practice? At its core, it is a tax strategy where your rental losses reduce your taxable income, meaning the tax office effectively subsidises part of the shortfall. It sounds simple until you try to calculate it against your own numbers. The mechanics involve more than just "losing money on purpose". You need to understand how loan interest, depreciation, and running [...] READ MORE