CGT Discount on Investment Property: How It Works in Australia

Selling an investment property can trigger a capital gains tax bill large enough to change your retirement plans or your next purchase decision. If you’ve held the property for more than twelve months, the CGT discount on investment property could cut that bill in half, but only if you meet the eligibility rules and structure the sale correctly.

This article explains exactly how the 50% CGT discount works for Australian property investors, who qualifies, and where people commonly get tripped up. We’ll cover the twelve month ownership test, how the discount interacts with your cost base calculations, and what happens when the property is held in a trust, company, or SMSF rather than your own name.

We’ll also walk through practical tax planning strategies you can use before settlement, including timing the sale, offsetting gains with losses, and knowing when it’s worth talking to your accountant before you sign a contract. After 35 years advising Melbourne property investors, we’ve seen the difference correct CGT planning makes to the final number on your tax return.

Why the CGT discount matters for property investors

Capital gains tax is calculated on your marginal tax rate, and for many property investors that rate sits at 37% or even 45% once the gain is added to their other income. Without the CGT discount, a $400,000 gain on an investment property could add roughly $148,000 to $180,000 to your tax bill in a single year. That’s the kind of number that forces people to sell other assets, delay retirement, or hand over a chunk of the deposit they were counting on for their next purchase.

The real cost of getting it wrong

Missing the discount, or structuring a sale so you don’t qualify for it, isn’t a small oversight. It’s often the single biggest tax event most property investors will ever face, bigger than the tax paid on years of rental income combined. We regularly meet clients who assumed the discount applied automatically, only to find out during tax time that a technicality, such as selling one day before the twelve-month mark, cost them tens of thousands of dollars.

Getting the CGT discount wrong on an investment property sale is often the most expensive mistake an investor will make in a single financial year.

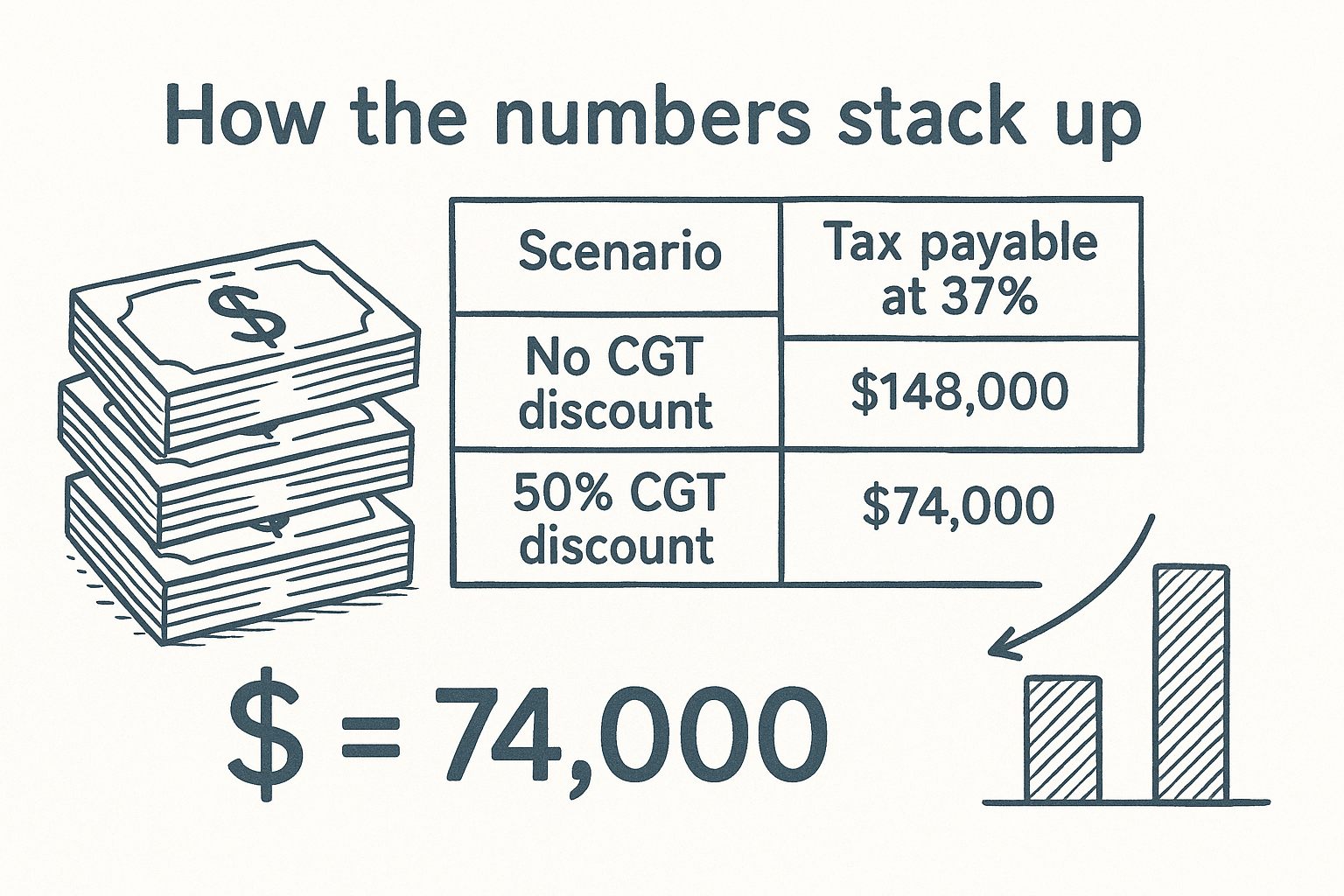

How the numbers stack up

The table below shows how dramatically the discount changes the outcome on a $400,000 capital gain, assuming a 37% marginal tax rate.

| Scenario | Taxable gain included in assessable income | Tax payable at 37% |

|---|---|---|

| No CGT discount applied | $400,000 | $148,000 |

| 50% CGT discount applied | $200,000 | $74,000 |

That’s a $74,000 difference from one eligibility test, the twelve-month ownership rule. No other single decision in the sale process moves the needle that far.

Why timing your sale matters

Ownership structure and settlement date both affect whether you get the discount at all, and by how much. A property held for eleven months and three weeks gets no discount whatsoever, even though it’s practically the same investment as one held for twelve months and one week. Settlement date, not exchange date, is generally what the Australian Taxation Office (ATO) uses to test the holding period, so a slow conveyancer or a delayed settlement can quietly push you outside the qualifying window in either direction.

Property investors who understand this early tend to plan their exit well before they list, rather than scrambling once an offer lands. Knowing the rules months in advance gives you room to negotiate settlement terms, choose the right financial year to sell in, and avoid a rushed decision that locks in a bigger tax bill than necessary. This is exactly where the discount stops being a theoretical tax concept and starts being a practical lever you can pull to protect the return on your investment property.

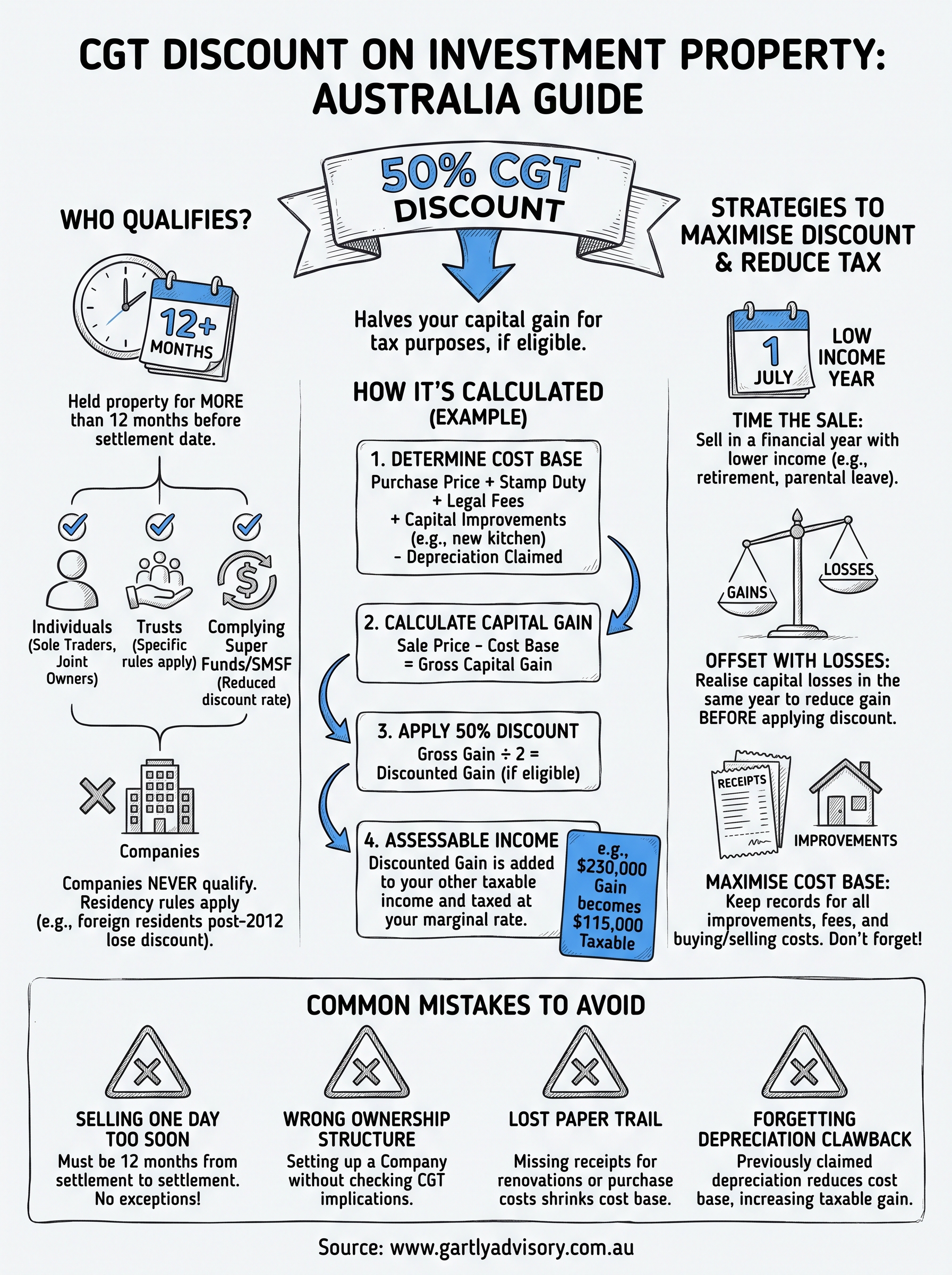

How to qualify for the 50% CGT discount

Qualifying for the 50% CGT discount isn’t automatic just because you sold at a profit. The Australian Taxation Office sets out specific tests around ownership length, entity type, and residency, and you need to pass all of them, not just the one everybody talks about.

The twelve-month ownership test

First, you must have owned the property for at least twelve months before the CGT event, which is generally the settlement date, not the date you signed the contract. Miss this by even a few days and the entire discount disappears, not just a portion of it. This is why sellers close to the anniversary of purchase should check the exact settlement timeline with their conveyancer before agreeing to a date.

Who can actually claim the discount

Not every ownership structure qualifies, even when the twelve-month test is met. Eligible entities include:

- Individuals, including joint owners and sole traders

- Trusts, though the discount flows through to beneficiaries under specific rules

- Complying superannuation funds, including SMSFs, at a reduced discount rate

Companies are excluded entirely, regardless of how long the asset was held.

Companies never receive the CGT discount, so the entity you buy an investment property through matters just as much as how long you hold it.

Residency and asset timing rules

Foreign residents and temporary residents generally lost access to the discount for gains accrued after 8 May 2012, which catches out investors who move overseas without checking their residency status at sale time. The property must also have been acquired after 20 September 1985, since assets bought before that date sit outside the CGT regime altogether. Getting these eligibility conditions confirmed early, ideally when you’re still deciding how to structure the purchase, avoids an unpleasant surprise when it’s time to sell.

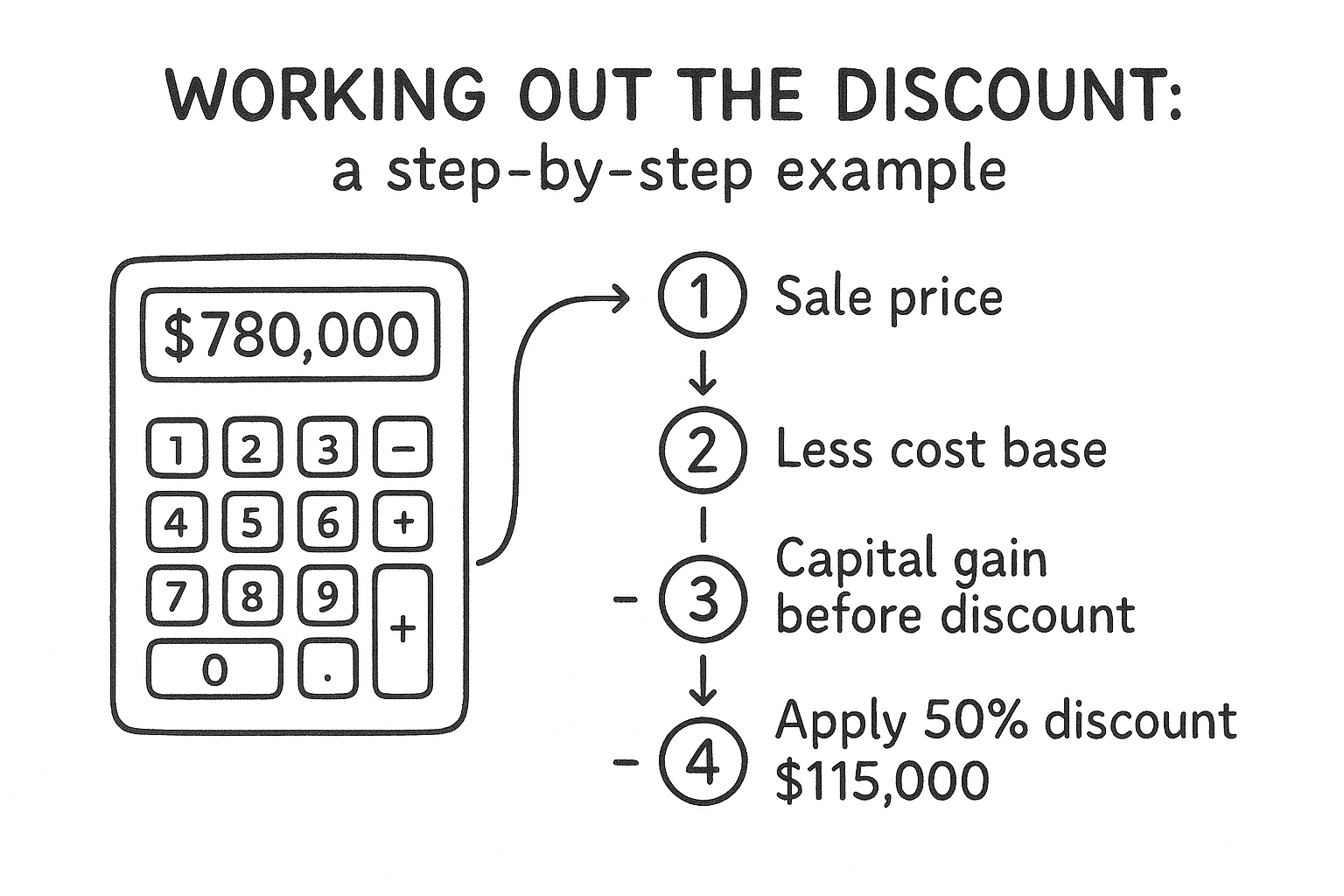

Working out the discount: a step-by-step example

Numbers make this rule easier to understand than any explanation of legislation. Take an investor who bought a rental property in Ormond for $500,000 in March 2019 and sold it for $780,000 in June 2024, five years later, comfortably clearing the twelve-month test.

Building the cost base first

Before you can calculate the gain, you need an accurate cost base, which includes more than the purchase price. Stamp duty, legal fees, and certain capital improvements all add to it, while depreciation claimed over the years reduces it.

| Item | Amount |

|---|---|

| Purchase price | $500,000 |

| Stamp duty and legal fees | $28,000 |

| Capital improvements (new kitchen) | $22,000 |

| Total cost base | $550,000 |

Applying the discount to the gain

With the cost base set at $550,000 and a sale price of $780,000, the raw capital gain sits at $230,000. Because the property was held for more than twelve months and owned in the investor’s own name, the 50% discount applies directly to that figure.

- Sale price: $780,000

- Less cost base: $550,000

- Capital gain before discount: $230,000

- Apply 50% CGT discount: $115,000

- Amount added to assessable income: $115,000

Halving a $230,000 gain to $115,000 before it even reaches your tax return is the entire purpose of the discount.

Why the order of operations matters

Investors sometimes apply the discount before deducting costs, or forget to add improvement costs to the base, and both errors change the final tax bill. Working through cost base calculations in the correct sequence, subtract first, then discount, keeps the figure accurate and defensible if the ATO ever asks questions. Once you’ve got that $115,000 figure, it’s added to your other taxable income for the year and taxed at your marginal rate, which is where the timing strategies in the next section start to matter.

Strategies to maximise your CGT discount

Once you’ve confirmed you qualify for the discount, the real work is minimising the gain it applies to, and controlling when that gain lands in your tax return. Smart timing and deliberate use of losses can shrink the final bill by tens of thousands of dollars, even after the discount has already been applied.

Time the sale around your income

Because the discounted gain is added to your other taxable income, selling in a year when your income is lower, say after retiring, taking parental leave, or between contracts, pushes less of the gain into the top tax brackets. Some investors settle a sale on 1 July rather than 30 June specifically to push the gain into the following financial year, buying themselves twelve extra months to plan for the tax bill or to time it against a lower-income year.

The tax you pay on a capital gain depends less on the gain itself and more on what else lands in your tax return that same year.

Offset gains with capital losses

If you’re holding other underperforming shares or assets, realising a capital loss in the same financial year as the property sale directly reduces the gain before the discount is even applied. This sequencing matters: losses offset the gain first, then the 50% discount applies to what’s left, so pairing a sale with a loss-making disposal can meaningfully cut the final figure.

Maximise your cost base

Every dollar you add to your cost base is a dollar removed from the taxable gain. Keep records of:

- Stamp duty and conveyancing fees paid on purchase

- Capital improvements, such as renovations, extensions, or new fencing

- Agent fees and marketing costs at sale

- Borrowing costs not already claimed as deductions

Missing receipts here is one of the most avoidable ways investors overpay tax, since the ATO won’t accept a cost you can’t substantiate.

Common mistakes that cost investors the discount

Even experienced investors trip over rules that seem straightforward on paper. The CGT discount on investment property rewards patience and paperwork, and small slip-ups in either area routinely cost thousands of dollars that a bit of planning would have saved.

Selling one day too soon

Almost every accountant has a client who sold a property eleven months and twenty-nine days after settlement, thinking the discount would still apply because "it’s close enough". It isn’t. The ATO counts from settlement date to settlement date, and there’s no rounding or goodwill allowance for near misses.

A single day inside the twelve-month window can be worth tens of thousands of dollars, so never leave the settlement date to chance.

Buying through the wrong structure

Trusts and individuals get access to the discount, but companies never do, no matter how long the property sits on the balance sheet. Investors who set up a company for asset protection reasons, without checking the CGT consequences first, often discover the mistake only when the accountant runs the numbers at sale time.

Losing the paper trail

Poor record keeping quietly erodes the discount by shrinking the cost base you’re entitled to claim. Common gaps include:

- Missing receipts for renovations completed years earlier

- No record of stamp duty or legal fees from purchase

- Undocumented borrowing costs

- Depreciation schedules that were never updated after improvements

Forgetting depreciation clawback

Property investors who claimed depreciation deductions over the years sometimes forget those amounts reduce the cost base, and therefore increase the taxable gain, at sale. Ignoring this adjustment leads to underreporting the gain, which creates a bigger problem than the tax saved, since the ATO can amend assessments and add penalties once the discrepancy surfaces.

Getting your next property sale right

The CGT discount on investment property rewards investors who plan ahead, not those who scramble after signing a contract. Get the twelve-month test right, hold the property through the correct structure, and keep every receipt from settlement to sale, and you’ll walk away with a materially smaller tax bill than someone who leaves it to chance.

Gartly Advisory has spent 35 years helping Melbourne property investors work through exactly these decisions, from choosing the right ownership structure before purchase to timing a sale around the financial year that suits your income. Every property, and every investor’s circumstances, throws up a slightly different answer to these rules.

Before you list your next investment property, get your cost base, ownership structure, and settlement timing checked properly. Book a consultation with Gartly Advisory and make sure the discount you’re entitled to actually lands on your tax return.

{kind=link}

{kind=link}

{kind=link}

{kind=link}