Company Tax Rate Australia: 25% or 30%, and Who Pays It

If you have ever stared at your company’s tax return wondering whether you should be paying 25% or 30%, you are not alone. The company tax rate australia businesses use depends entirely on whether you qualify as a base rate entity, and plenty of directors get this wrong or assume last year’s rate still applies without checking.

Here is the short answer: most small and medium businesses pay 25%, while larger companies and those earning too much passive income pay 30%. The test comes down to your aggregated turnover and how much of your income is base rate entity passive income, not simply how big your business feels.

In this article, we will walk through both current tax rates, explain the base rate entity eligibility rules in plain terms, and show you how to work out which one applies to your company. We will also cover common mistakes business owners make when self-assessing their rate, so you can lodge with confidence and avoid a nasty surprise from the ATO.

Why the company tax rate matters for your business

Getting your company tax rate right is not just an admin detail, it directly changes how much cash stays in your business at the end of the year. A five-percentage-point gap between 25% and 30% might sound small, but on $500,000 of taxable profit that is $25,000 difference, enough to cover a new hire, a marketing push, or a chunk of equipment finance. For growing businesses, that gap compounds every year you get it wrong.

Cash flow and reinvestment capacity

Beyond the immediate tax bill, your rate affects how much retained profit you have available to reinvest without needing a loan or drawing on the owners’ pockets. Businesses paying 30% instead of the 25% base rate entity rate effectively hand over an extra slice of every dollar earned, money that could otherwise fund stock, staff training, or a second location. Over a five-year growth phase, this difference can genuinely decide whether you self-fund expansion or stay reliant on debt.

Franking credits and shareholder returns

Your company tax rate also determines the franking credits attached to dividends you pay shareholders, and this is where a lot of directors get caught out. The franking rate is tied to your corporate tax rate for imputation purposes, which is based on your prior year’s aggregated turnover and base rate entity status, not necessarily the rate you expect to pay this year. Pay dividends using the wrong franking rate and shareholders can end up under-credited or over-credited, triggering amendments and awkward conversations at tax time. The Australian Taxation Office sets out the corporate tax rate for imputation purposes clearly on its website, and it is worth checking every single year rather than assuming last year’s setting still holds.

A five-point gap between 25% and 30% on $500,000 of profit is $25,000, real money that changes what you can reinvest or distribute.

The cost of getting it wrong

Misapplying your rate does not just cost you cash, it creates compliance headaches that eat into the time you should be spending running your business. Common consequences include:

- Amended assessments from the ATO once your actual aggregated turnover is confirmed

- Interest charges on any shortfall between what you paid and what you owed

- Franking account problems if dividends were franked at the wrong rate

- Cash flow shocks when a correction lands months after you thought the year was closed

None of these outcomes are catastrophic on their own, but stacked together they distract from the real work of growing your business. Understanding why the rate matters is the first step; the next is working out, methodically, which rate actually applies to you.

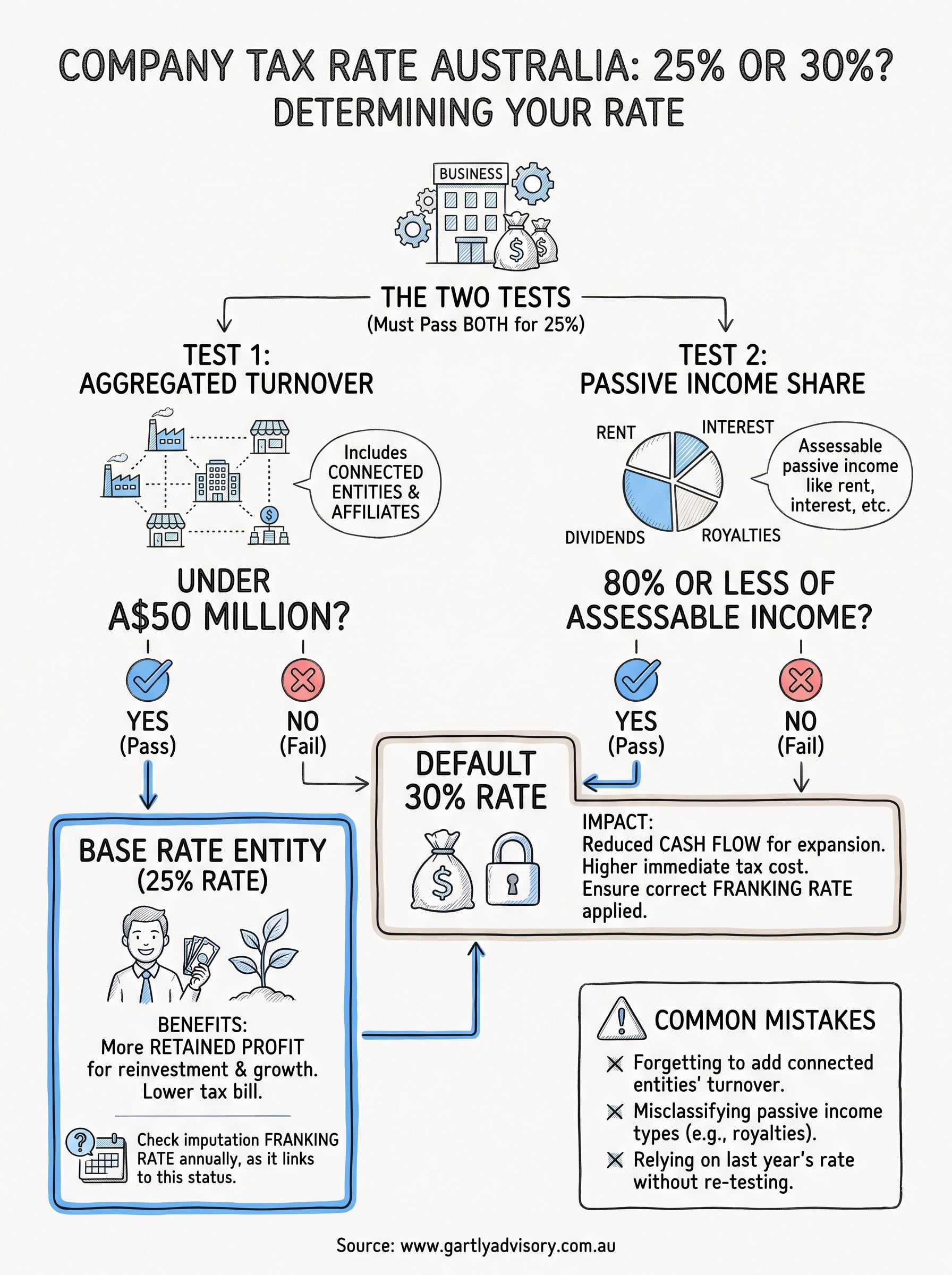

How to work out which rate applies to your company

Working out your company tax rate comes down to two tests, and you need to pass both to land on the 25% base rate entity rate. The first test looks at your aggregated turnover, which is your business’s annual turnover combined with the turnover of any connected entities or affiliates. The second test checks how much of your income counts as base rate entity passive income, things like dividends, interest, rent, royalties, and net capital gains. Miss either test and you default to the 30% rate, regardless of how small your operation feels.

Step 1: Check your aggregated turnover

Your aggregated turnover must sit under $50 million for the income year to even be eligible for the lower rate. This threshold catches most small and medium businesses comfortably, but franchise groups, related trusts, and businesses with common ownership structures can easily push combined turnover over the line without realising it. Add up turnover across every connected entity before you assume you qualify.

Step 2: Test your passive income

Even if your turnover is well under the threshold, your business fails the base rate entity test if more than 80% of your assessable income is passive income. This rule exists specifically to stop investment companies and holding structures from claiming a small business tax concession they were never meant to access. If rental income, dividends, or interest make up the bulk of what you earn, check this percentage every year, because it can shift quickly.

Passing the turnover test means nothing if more than 80% of your income is passive, so check both tests every single year.

| Test | Threshold | Result if failed |

|---|---|---|

| Aggregated turnover | Under $50 million | Defaults to 30% |

| Passive income share | 80% or less of assessable income | Defaults to 30% |

The Australian Taxation Office publishes detailed guidance on both tests, and it is worth reviewing annually rather than relying on your accountant’s assumption from the previous year. Turnover and income mix both shift as your business grows or changes structure.

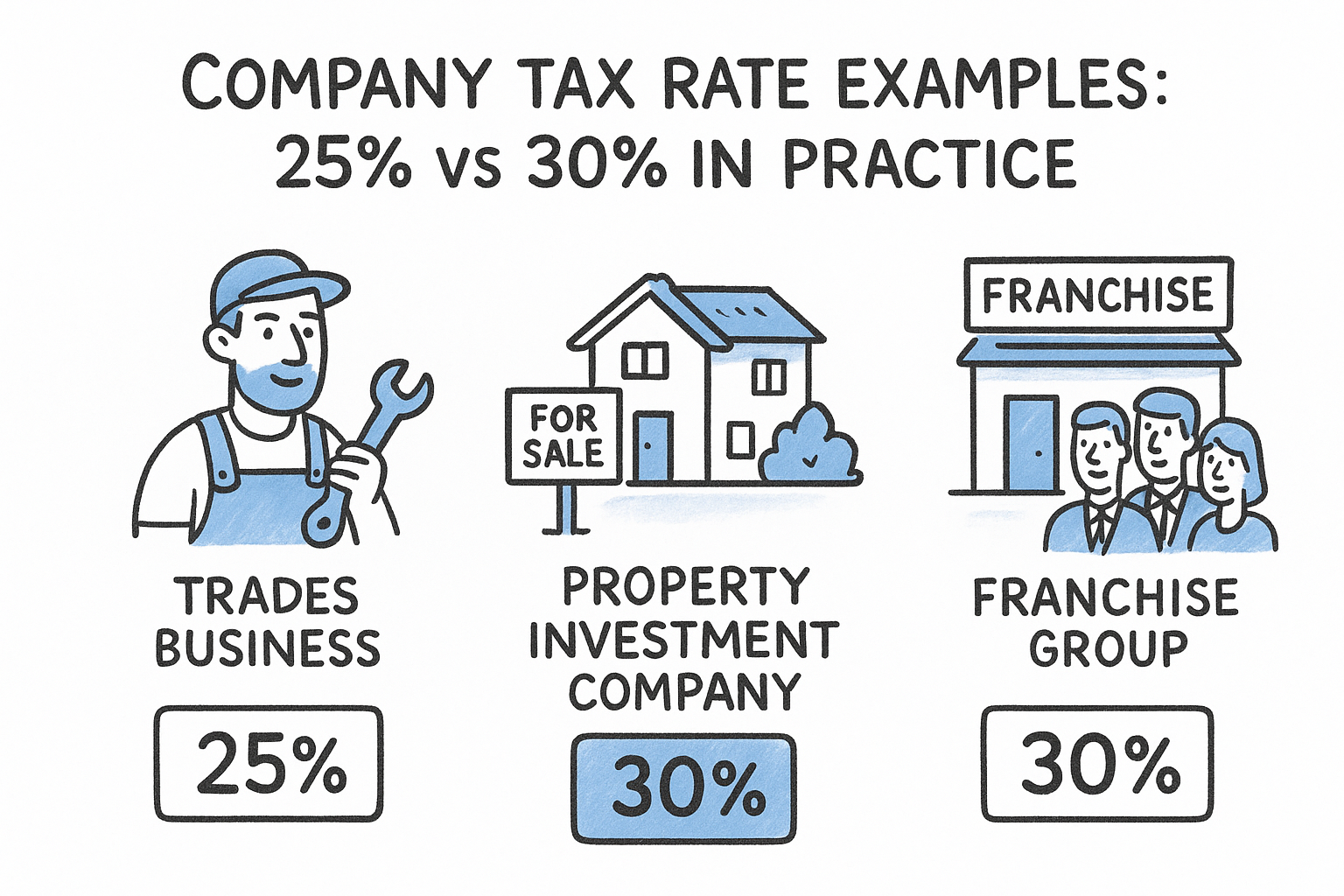

Company tax rate examples: 25% vs 30% in practice

Numbers make this rule click faster than definitions ever will. Take three businesses with different turnover and income mixes, and you can see exactly why the base rate entity test matters more than gut feel about how "small" a business seems.

Example 1: The trades business

Geoff runs a plumbing business with $2 million aggregated turnover, almost all of it from client invoices. Practically none of his income is passive, so he clears both tests easily and pays the 25% company tax rate. On $300,000 taxable profit, that is $75,000 in tax rather than $90,000, a $15,000 saving he ploughs straight back into a second van and an apprentice’s wages.

Example 2: The property investment company

A company holding three rental properties earns $180,000 a year, almost entirely rent and a small capital gain from a sale. Turnover sits well under $50 million, but rent and the capital gain push passive income past 80% of total assessable income. Despite being tiny by turnover standards, this company fails the passive income test and pays 30%, not 25%.

Example 3: The franchise group

A franchisee turning over $8 million individually looks comfortably under the $50 million threshold. But once you add the turnover of two related franchise entities under common ownership, aggregated turnover climbs to $52 million. That single connection tips the group into the 30% bracket for every entity involved, even the smallest one.

Turnover under $50 million means nothing on its own, a company earning $180,000 can still pay 30% if most of that income is passive.

| Business | Turnover | Passive income share | Rate applied |

|---|---|---|---|

| Plumbing business | $2 million | Low | 25% |

| Property investment company | $180,000 | Over 80% | 30% |

| Franchise group (aggregated) | $52 million | Low | 30% |

Each case passes or fails on a different test, which is exactly why checking both every year matters more than assuming last year’s rate still fits.

Common mistakes that tip businesses into the higher rate

Most directors do not deliberately misapply their company tax rate, they simply overlook a detail that shifts the outcome. These slip-ups are predictable, which means they are also avoidable if you know where to look before you lodge.

Forgetting connected entities

Business owners frequently calculate turnover using only their own entity’s figures, ignoring related trusts, companies, or partnerships under common control. The aggregated turnover rules require you to add in any connected entity or affiliate, and a group that looks small on paper can quietly cross the $50 million threshold once everything is combined. If you run more than one entity, or share ownership with a related business, add up the whole group before you assume you qualify for 25%.

Misclassifying passive income

Rental income, interest on a business loan account, and royalties often get lumped in with ordinary trading income without a second look. That is a costly assumption, because base rate entity passive income is defined specifically by the ATO, and getting the classification wrong can push you over the 80% threshold without you noticing until an amendment lands.

Overlooking one connected entity or misreading your passive income mix is usually all it takes to lose the 25% rate.

Relying on last year’s rate

Your eligibility is assessed fresh every income year, not carried over from the last one. A business that grew turnover, sold an investment property, or restructured ownership can move from 25% to 30% without anyone updating the assumption in the tax return software.

A quick self-check before you lodge

Run through this list before finalising your return:

- Add up turnover across every connected and affiliated entity, not just your own

- List every passive income source, including rent, interest, dividends, royalties, and capital gains

- Calculate the passive income percentage against total assessable income

- Confirm the current year’s figures, since last year’s rate is not a guarantee

- Check franking rates applied to any dividends against the correct imputation rate

A few minutes on this checklist beats an amended assessment months later.

Getting your company tax rate right

Working out your company tax rate is not guesswork, it is two tests applied fresh every year: aggregated turnover under $50 million, and passive income at or below 80% of assessable income. Pass both and you sit at 25%. Fail either one and you default to 30%, no matter how small your business feels. The examples above show how easily a connected entity or a spike in rental income can flip the outcome without you noticing.

Getting this wrong costs real money, whether through overpaid tax, an amended assessment, or a franking mismatch that unsettles your shareholders. Running the self-check before you lodge takes minutes and saves months of correction later.

If you would rather have a specialist confirm your base rate entity status and structure your business for the lowest legitimate rate, talk to the team at Gartly Advisory before your next lodgement is due.

{kind=link}

{kind=link}

{kind=link}

{kind=link}