– Hero Image")

Business Structure Advice: Sole Trader vs Company (2026 Australian Guide)

The simplest business structure might actually be your most expensive mistake once your annual profit climbs past A$120,000. While starting as a sole trader is easy, staying one for too long often means you’re paying thousands in unnecessary tax while leaving your family home vulnerable to business risks. You’ve likely felt that sting when looking at your last ATO assessment, wondering why you’re being taxed at high individual rates. You aren’t alone in wanting a safer foundation for your future. Our team has spent 25 years providing the business structure advice sole trader vs company owners rely on to move beyond the numbers and find a setup that actually supports their growth.

We’re here to help you secure a tax-efficient setup for 2026. You’ll discover the exact A$150,000 financial threshold where switching to a company becomes a necessity rather than a choice. We’ll also clarify confusing ASIC compliance rules so you can enjoy genuine peace of mind regarding asset protection. This article compares tax rates, setup costs, and legal safeguards to ensure your hard work stays in your pocket.

Key Takeaways

- Understand the fundamental shift from being your business as a sole trader to creating a separate legal entity, and why 2026 is the perfect time to evaluate if your current structure still supports your long-term goals.

- Learn how to protect your most valuable personal assets, like the family home, by moving away from the “all-in” risk of a sole trader setup and utilizing the asset protection benefits of the “Corporate Veil.”

- Navigate the complexities of the Australian tax system with expert business structure advice sole trader vs company to determine if you are eligible for the 25% small business tax rate and other flexibility benefits.

- Pinpoint the exact financial “tipping point”-typically when profits reach the A$120,000 to A$150,000 range-where the tax savings and liability protection of a company structure begin to outweigh the administrative costs.

- Discover the value of having a proactive partner like Geoff Gartly, who brings 35 years of experience to help you look beyond the numbers and transition your business with confidence and clarity.

The Starting Line: Choosing Between a Sole Trader and a Company Structure

Starting a business in Australia feels like a sprint, but your structure is a marathon decision. The core choice boils down to whether you want to be the business or own the business. If you operate as a sole trader, you and the enterprise are a single legal entity. This means your personal assets, like your family home or your personal savings, are on the line if the business faces a lawsuit or debt. A company changes this dynamic entirely by creating a separate legal person under the law.

We’ve seen a 12% increase in clients seeking business structure advice sole trader vs company as we look toward 2026. This period is a critical milestone because the Australian Taxation Office (ATO) is tightening rules around professional firm profit allocation and the use of discretionary trusts. By June 2026, many legacy structures will need a total overhaul to remain compliant and tax-effective. Reviewing your setup now prevents you from being stuck in an outdated model that no longer serves your growth goals.

Don’t let your ABN lead you into a false sense of security. Holding an Australian Business Number is a tax requirement; it offers zero protection against personal liability. Many new entrepreneurs choose simplicity to avoid the A$597 ASIC registration fee, but they often regret this choice when they try to hire their first employee or lease a commercial space. While a sole trader setup is easy to manage, it lacks the scalability required for a multi-person team. If you plan to scale, starting as a company can save you the headache of transferring assets and contracts later on.

What is a Sole Trader?

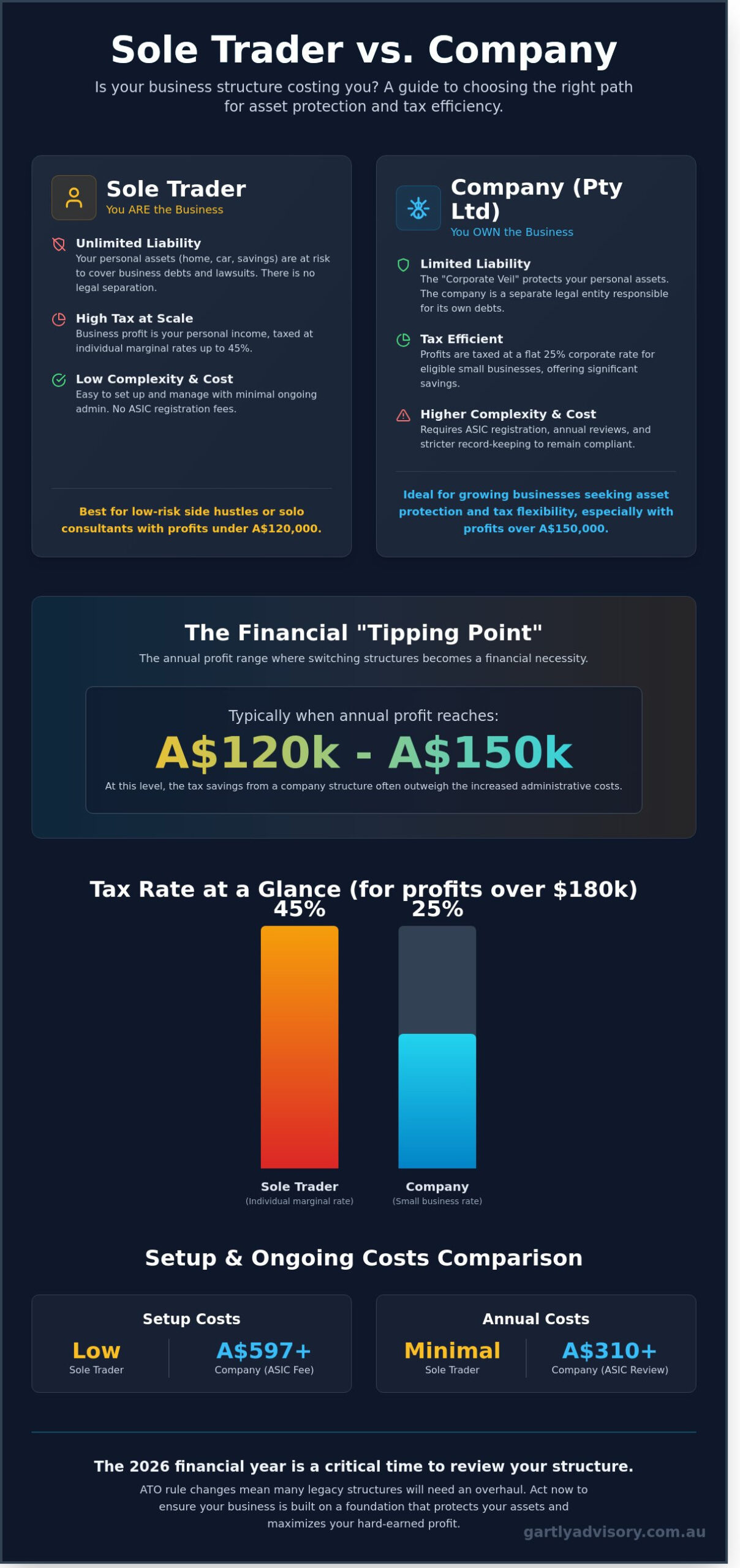

This is the most straightforward way to trade. You use your individual Tax File Number and report all business income on your personal tax return. If you follow the Sole Trader Path, you enjoy total control and very low setup costs. However, you’re taxed at individual marginal rates. For high earners, this can mean losing 45% of every dollar to tax once you cross the top threshold. It’s an excellent choice for low-risk side hustles or solo consultants with minimal overheads.

What is a Proprietary Limited (Pty Ltd) Company?

A Pty Ltd company is a separate legal person created under the Corporations Act 2001. It owns its own money, pays its own tax (usually at a 25% rate for small businesses), and carries its own debts. Shareholders own the equity, while directors manage the daily operations. This structure offers superior asset protection but comes with higher hurdles. You’ll need to pay the A$310 annual ASIC review fee and keep detailed records of all meetings and financial transactions to meet your corporate governance duties.

Choosing the right path requires looking beyond the immediate costs. If your profit is likely to exceed A$120,000 in the 2026-27 financial year, the tax flexibility of a company often justifies the extra paperwork. At Gartly Advisory Pty Ltd, we love helping our clients find that “sweet spot” where protection and tax efficiency meet. Let us be your partner in determining which foundation will support your dreams for the next decade.

The Sole Trader Path: Low Complexity, High Personal Liability

Starting as a sole trader is the most common entry point for Australian entrepreneurs. Data from the Australian Bureau of Statistics suggests that over 60% of small businesses operate without employees, and a vast majority of these begin as sole traders. It’s popular because you don’t need a separate Tax File Number (TFN) for the business; you just use your personal one. You’ll likely only need to register for Goods and Services Tax (GST) once your turnover hits the A$75,000 threshold. While this sounds easy, the simplicity masks a significant danger that many ignore until it’s too late.

You and your business are legally the same person. This means your liability is unlimited. If your business faces a legal dispute or cannot pay its debts, your personal assets are on the line. Your car, your savings, and even your family home can be seized to satisfy business obligations. This Australian government source highlights how this lack of protection is a primary drawback. When you seek business structure advice sole trader vs company, this risk is usually the first thing a professional will flag. It’s a heavy price to pay for a structure that costs almost nothing to set up.

Growth also hits a ceiling quickly under this model. Banks often hesitate to lend large sums to individuals without a corporate history or clear separation of assets. Investors almost never put money into a sole trader setup because there are no shares to issue. You’re effectively the engine and the fuel; if you stop working due to illness or injury, the business stops with you. This makes the entity very difficult to sell in the future.

Financial Simplicity and Cash Flow

Cash flow is straightforward because there’s no legal requirement to pay yourself a “wage” in the traditional sense. You simply take “drawings” from the profit as you need them. However, this flexibility often leads to a retirement trap. Many sole traders forget to set aside the current 11.5% superannuation guarantee rate for themselves. Without a disciplined approach, you might reach retirement with a significant financial gap. You do benefit from the A$18,200 tax-free threshold, which helps in the early days of low profit. If you’re feeling overwhelmed by these moving parts, you can talk to our team for a clearer perspective on your numbers.

The Hidden Costs of Staying Small

Operating as an individual brings invisible hurdles that can stifle a growing brand. In many Australian states, sole traders can’t cover themselves under their own workers’ compensation insurance. You’d need private income protection, which often costs more than a standard policy. Tax is another hurdle. You pay tax at your individual marginal rate, which can climb as high as 45% plus the Medicare levy for high earners. Unlike a company, you can’t “park” profits inside the business at a lower corporate rate for future investment. Every dollar you earn is taxed in the year you earn it, leaving less capital for a rainy day. This lack of retained earnings makes it much harder to scale up when a big opportunity suddenly appears.

The Company Route: Asset Protection and Tax Flexibility

Stepping into a company structure is a significant milestone for any Australian entrepreneur. While a sole trader is the simplest path, a proprietary limited (Pty Ltd) company offers a layer of security that’s hard to ignore as your turnover climbs and your risk profile changes. This is where business structure advice sole trader vs company becomes essential for long-term wealth preservation and strategic growth.

The defining feature of this structure is the “Corporate Veil.” This legal concept treats the company as a separate person in the eyes of the law. If the business incurs a debt or faces a legal claim, the creditors generally can’t touch your personal bank account, your car, or the family home. To formalise this separation, you must register with the official company registration body, which establishes your business as a distinct entity. This barrier provides a level of peace of mind that a sole trader simply doesn’t have.

Tax efficiency is another major driver for this transition. For the 2023-24 financial year, base rate entities with an aggregated turnover of less than A$50 million enjoy a flat 25% tax rate. Compare this to the personal marginal tax rates, which can climb as high as 47% for individuals earning over A$190,000. By using a company, you control when you receive income. You can keep profits within the business to reinvest, rather than being forced to pay personal tax on every dollar the business earns in a single year.

Credibility also plays a role in your market positioning. Many larger Australian corporations and government departments have procurement policies that prefer, or even require, dealing with “Pty Ltd” entities. It signals a level of permanence and regulatory oversight. When you’re pitching for a contract worth A$500,000, having a company structure often acts as a prerequisite for being taken seriously by the “big end of town.”

Succession planning is significantly cleaner under this model. Because a company has perpetual succession, it doesn’t die with the owner. Selling the business involves a transfer of shares. The contracts, leases, and employee agreements remain with the entity, making the transition seamless for a buyer. This often leads to higher valuations compared to a sole tradership where the business is often inextricably linked to the individual.

Asset Protection Strategies

We often guide our clients to separate “risk” from “wealth.” In this model, the company operates the business and carries the risk, while your family home is held in a different name or a family trust. You must be diligent, however. Under Section 588G of the Corporations Act 2001, directors can be held personally liable for “insolvent trading.” If you don’t manage your cash flow and allow the company to incur debts it can’t pay, the corporate veil won’t protect you. You should also expect that banks will require personal guarantees for any business loans, which bypasses some of the structural protections for those specific debts.

Tax Planning and Profit Distribution

Companies offer sophisticated ways to manage how you’re paid. Through franking credits, the ATO ensures you aren’t double-taxed. When the company pays its 25% tax and then pays you a dividend, you receive a credit for the tax already paid. This is a core part of business structure advice sole trader vs company. You can also pay yourself a market-rate salary plus superannuation, just like any other employee. Any remaining profit can stay in the company as retained earnings. This allows you to build a “war chest” for future expansion or to weather a quiet period without triggering a high personal tax bill.

The Tipping Point: When to Transition from Sole Trader to Company

Deciding when to move from a sole trader setup to a proprietary limited company is a milestone for any growing Australian business. It’s rarely about a specific date on the calendar. Instead, it’s about when the benefits of a corporate structure outweigh the increased compliance costs. For most of our clients at Gartly Advisory, this shift happens when net profit consistently lands between A$120,000 and A$150,000. At this level, the tax savings often exceed the A$310 ASIC annual review fee and the higher accounting costs associated with company tax returns.

Risk is the other major driver for this change. If you’re signing contracts worth more than A$250,000 or working in high-risk industries like construction or heavy engineering, the “corporate veil” becomes essential. As a sole trader, your personal home and savings are on the line if a legal dispute arises. A company structure limits this liability, protecting your family’s assets while you grow your dreams. It’s a proactive step that moves you from a simple job to a scalable business asset.

The Financial Math of Switching

In the 2024-25 financial year, individual tax rates include a 37% bracket for income over A$135,000. By contrast, a base rate entity company pays a flat 25% tax on profits. By 2026, even with adjusted tax scales, the ability to “cap” tax at 25% and retain earnings within the business for future growth remains a powerful strategy. You should also consider superannuation. High-income earners benefit from the 15% concessional tax rate on contributions, which is often easier to manage through a company payroll system. We often see clients save upwards of A$12,000 in annual tax by making the switch at the right time. You must factor in the setup costs, which typically range from A$1,500 to A$3,000 depending on the complexity of your requirements.

Understanding Personal Services Income (PSI)

The ATO’s PSI rules are a common trap for IT consultants, engineers, and creative professionals. If more than 50% of your income is a reward for your personal skills or efforts, the ATO might ignore your company structure for tax purposes. To bypass this, you must pass the “Results Test.” This means you’re paid to produce a specific outcome, you provide your own tools, and you’re liable for the cost of fixing any defects. Roughly 60% of independent contractors fail the 80% rule, where too much income comes from a single source. Getting expert business structure advice sole trader vs company early ensures you don’t build a structure that the ATO simply looks through. We help you structure your contracts and workflow to meet these tests head-on.

Moving assets like equipment or intellectual property into a new company counts as a sale at market value. While the Small Business CGT concessions under Division 152 can potentially reduce this liability to zero, the paperwork must be exact. It’s a complex transition that requires a safe pair of hands to navigate correctly without triggering an unexpected tax bill. We look beyond the numbers to ensure your transition is seamless and legally sound.

Ready to see if the math adds up for your business journey? Talk to us and let us help you find your tipping point today.

Beyond the Numbers: Strategic Advice with Gartly Advisory

A simple ABN registration might get your doors open, but it won’t protect your family home or prepare you for a future sale. Melbourne’s ambitious SMEs need more than a generic template they found online. Choosing the right path requires business structure advice sole trader vs company that considers where you want to be in a decade, not just where you are today. Geoff Gartly brings 35 years of experience in business transition to every conversation. He’s seen how a poorly chosen structure can cost a founder A$60,000 or more in unnecessary capital gains tax when they eventually exit their venture.

Geoff’s 35-year track record means he’s guided local businesses through the 2008 financial crisis and the 2020 pandemic lockdowns. He understands that your business isn’t just a source of income; it’s a vehicle for your family’s security. Our ‘Trusted Partner’ approach means we look at your estate planning and family goals alongside your tax returns. We don’t just crunch numbers. We build a fortress around your assets so that your personal wealth remains insulated from business risks.

We handle the heavy lifting that usually keeps business owners awake at night. From managing your ASIC company registration to configuring your Xero file with a customised chart of accounts, we ensure the technical foundation is flawless. You won’t have to worry about missing a deadline or filing the wrong form. Our team takes care of the administrative burden so you can focus on growing your revenue and serving your customers.

The Gartly Advisory Difference

We provide advice that goes beyond the numbers by aligning your current structure with your eventual exit planning. If you intend to sell your business by 2030, the decisions you make in 2024 are vital for accessing the small business CGT concessions. You aren’t just another entry in a digital portal; you’re a Melbourne business owner who gets real, face-to-face support. We offer complementary initial consultations for structure reviews because we believe every entrepreneur deserves a safe pair of hands to guide them. Our 70+ 5-star Google reviews reflect our commitment to being proactive partners rather than just reactive accountants.

Your Roadmap to a Secure Structure

Our process is methodical and designed to eliminate guesswork. We follow a three-step journey to ensure your business is positioned for success:

- Step 1: The Discovery session. We dive deep into your specific risk profile. If you’re in a high-risk industry like commercial construction, we prioritise asset protection. We listen to your goals for the next five years to see if a company or a trust provides the best flexibility.

- Step 2: Customised structure report. We provide a detailed comparison using your actual or projected 2024 figures. This report shows the exact tax differences in our business structure advice sole trader vs company analysis, allowing you to see the A$ value of your decision before you commit.

- Step 3: Seamless implementation. Once you’ve chosen your path, we execute the plan. This includes registering your company, applying for a new TFN and ABN, and setting up your Xero accounting software. We provide ongoing compliance support to ensure you stay on the right side of the ATO and ASIC.

Reliability is the cornerstone of our firm. With 25 years of established trust in the Melbourne community, we’ve helped hundreds of clients transition from simple setups into sophisticated, tax-effective companies. We love the opportunity to support our clients as they grow from a single-person operation into a thriving team. Talk to us today and let us help you build a business structure that lasts a lifetime.

Taking the Next Step in Your Business Journey

Deciding between staying a sole trader or moving to a company structure isn’t just about tax rates; it’s about protecting what you’ve built. While the sole trader path offers low complexity, it leaves your personal assets exposed. Transitioning to a company provides a legal shield and unlocks strategic tax flexibility as your revenue grows. Getting the right business structure advice sole trader vs company ensures you don’t pay more tax than necessary or risk your family home.

At Gartly Advisory, we bring 35 years of Chartered Accounting experience to your kitchen table or boardroom. We’ve helped hundreds of Melbourne entrepreneurs navigate these exact turning points. Our 70+ 5-star Google reviews reflect our commitment to being more than just accountants. We’re your partners in growth. Whether you’re just starting or you’ve hit that tipping point where a company structure makes more sense, we’ll guide you through the transition with calm competence. We love the opportunity to support our clients through every stage of their business life cycle.

Book a complimentary appointment with our Melbourne team to review your business structure. Let’s work together to build a secure foundation for your future success.

Frequently Asked Questions

Is it expensive to change from a sole trader to a company in Australia?

Moving from a sole trader setup to a proprietary limited company involves several upfront costs, starting with the ASIC registration fee of A$597 for the 2024/25 financial year. You’ll also need to budget for professional advice to ensure you don’t trigger unnecessary capital gains tax or stamp duty liabilities during the transition. Most small business owners spend between A$2,500 and A$5,500 on total setup costs, which includes legal documents, tax registrations, and strategic business structure advice sole trader vs company comparisons. While these initial figures might seem high, the long term benefits of asset protection and a capped 25 percent tax rate for base rate entities often outweigh the starting price. We’ve seen clients save over A$12,000 in tax in their first year alone by making this move at the right time.

You should also consider the ongoing compliance costs that come with a company structure. Unlike a sole trader who might only need a simple tax return, a company requires annual financial statements and a separate tax return which typically costs at least A$2,000 per year. There’s also the annual ASIC review fee to keep the company active. If you’re turning over more than A$150,000, these costs are usually seen as a necessary investment for growth. We help you look at the numbers to see if your current profit levels justify the shift. It’s about making sure the tax savings and risk reduction actually put more money back in your pocket after all the professional fees are paid.

Can I use the same ABN if I switch to a company structure?

No, you can’t use your existing ABN because a company is a completely separate legal entity from you as an individual. When you operate as a sole trader, the ABN is tied to your personal tax file number; however, a company is its own “person” in the eyes of the law and requires its own unique ABN and Tax File Number. You’ll need to apply for these through the Australian Business Register once your company is incorporated. This process marks a clean break between your personal affairs and the business’s financial obligations. It’s a common mistake to keep using the old ABN on invoices, but doing so can lead to significant issues with the ATO during an audit and might even void your limited liability protection.

Once your new company ABN is active, you’ll generally need to cancel your sole trader ABN unless you plan to keep a separate side project running under your own name. You’ll also need to update your GST registration and WorkCover policies to reflect the new entity. This is a critical step in the business structure advice sole trader vs company transition because it affects how you report your Business Activity Statements. If you accidentally claim GST credits under the wrong ABN, the ATO will likely flag the discrepancy. We recommend a “cutoff date,” usually the start of a new quarter or financial year, to make the switch clean. This ensures your record keeping remains spotless and your transition to the new structure is as smooth as possible for your customers and suppliers.

Do I need a separate bank account for a company?

Yes, it’s a legal requirement under the Corporations Act 2001 to keep company funds strictly separate from your personal money. Since the company’s money doesn’t belong to you personally, but rather to the company itself, you can’t simply pay for groceries or personal rent out of the business account. Opening a dedicated business transaction account in the company’s name is one of the first things you must do after receiving your Certificate of Registration. This clear separation is vital for maintaining the “corporate veil,” which is the legal barrier that protects your personal assets from business creditors. If you mix your funds, a court might decide the company is just an extension of yourself, potentially putting your family home at risk if the business faces legal action.

Having a separate account also makes your end of year accounting much simpler and cheaper. When we see a clean bank feed with only business transactions, it takes far less time to prepare your financial statements. You’ll pay yourself a formal wage or a dividend, which is then transferred from the company account to your personal account. This creates a clear paper trail for the ATO and shows that you’re operating with professional integrity. Most Australian banks like CBA or Westpac offer specialized business accounts with integrated accounting software links. Using these tools helps you track your 25 percent tax set asides and superannuation obligations in real time. It’s a foundational habit that separates successful entrepreneurs from those who struggle with cash flow management.

How much are the ASIC annual review fees in 2026?

Based on current indexation trends and the 3.8 percent increase seen in recent years, the ASIC annual review fee for a proprietary company is projected to be approximately A$341 in 2026. This fee is adjusted every July 1st in line with the Consumer Price Index. It’s a mandatory payment that keeps your company registered and active on the national database. While A$341 is the standard fee, it’s important to remember that late payments attract heavy penalties. If you pay even one day late, ASIC currently charges a A$93 penalty, which jumps to A$387 if the payment is more than one month overdue. We always advise our clients to set up a direct debit or pay via BPAY as soon as the annual statement arrives to avoid these unnecessary costs.

The annual review is more than just a fee; it’s a chance to confirm that your company’s details are accurate. You’ll receive an annual statement from ASIC around the anniversary of your company’s incorporation. You’re required to check that the directors’ addresses, shareholder details, and registered office address are all correct. If you’ve moved house or changed shareholders during the year and didn’t notify ASIC within 28 days, you might face additional “late lodgement” fees of A$93 or more. Keeping these details updated is part of your director’s duties. We often act as the registered office for our clients to ensure these documents are handled promptly. This proactive approach ensures you never get hit with surprise fines and that your company remains in good standing with the regulator.

What happens to my existing business name when I move to a company?

Your existing business name doesn’t automatically move to the company, so you’ll need to manually transfer it through the ASIC Connect portal. If you’ve been trading as “Sunshine Coast Plumbing” as a sole trader, that name is currently linked to your personal ABN. To move it, you first need to request a “transfer key” from ASIC. Once you have your new company ABN, you can use that key to register the name under the company’s ownership. The cost for this is A$42 for one year or A$98 for three years. It’s a straightforward process, but timing is everything. You don’t want to cancel the name under your sole trader ABN until you’re ready to immediately register it under the company, otherwise someone else could potentially swoop in and claim it.

It’s also worth noting that if your company name is exactly the same as your business name, you might not need to register a separate business name at all. For example, if your company is registered as “Sunshine Coast Plumbing Pty Ltd,” you can trade under that full name without extra registration. However, if you want to drop the “Pty Ltd” on your signage and website, the business name registration is still required. We see many clients use this transition as an opportunity to refresh their branding or protect multiple names under the one company umbrella. We can help you navigate the ASIC portal to ensure your intellectual property is protected. This ensures your customers still recognize your brand while you benefit from the more robust legal structure of a company.

Can a company own my car and equipment for tax purposes?

Yes, a company can certainly own your vehicles and machinery, and this is often a smart move for maximizing depreciation claims. Under the current tax rules, a company can claim a deduction for the decline in value of business assets like utes, vans, and specialized tools. If the vehicle is used 100 percent for business, the company pays for all fuel, insurance, and servicing, and then claims these as tax deductions. However, you need to be careful with Fringe Benefits Tax (FBT) if you’re also using the car for personal trips. The FBT rate is currently 47 percent, which can be quite expensive if not managed correctly. Many directors use the “logbook method” for 12 weeks to prove their business usage percentage and reduce the FBT liability to a manageable level.

For equipment like laptops, excavators, or office furniture, the company structure offers great flexibility. The company buys the asset, and it sits on the company’s balance sheet rather than yours. This is a key part of the business structure advice sole trader vs company discussion because it affects your personal “at risk” assets. If the company owns the equipment and the business fails, those assets might be sold to pay creditors, but your personal car or home stays safe. We also look at the “instant asset write off” thresholds, which change frequently based on the federal budget. For the 2024/25 year, the threshold is A$20,000 for small businesses. This allows you to get an immediate tax break on smaller equipment purchases rather than spreading the deduction over several years. We help you calculate whether it’s better to own the car personally and claim cents per kilometer or have the company own it outright.

Should I use a family trust in conjunction with my company?

Using a family trust to hold the shares of your company is a very common and effective strategy for both asset protection and tax planning. Instead of you owning the shares in your own name, the trust owns them. This means that when the company makes a profit and pays a dividend, that money goes into the trust. You can then distribute those dividends to various family members who might be in lower tax brackets. For example, if you have a child over 18 at university with no income, the trust could distribute some of the company profits to them, potentially saving thousands in tax compared to you taking all the income yourself at the top marginal rate. It’s a powerful way to manage family wealth while keeping the business operations separate.

The asset protection benefits are just as significant. Because you don’t personally “own” the company shares (the trust does), those shares are generally harder for creditors to reach if you’re personally sued. This adds an extra layer of security for your family’s future. However, you must be aware of Division 7A of the Income Tax Assessment Act. This rule prevents you from simply taking “loans” from the company to the trust without a formal agreement and market interest rates. If you get this wrong, the ATO will treat the money as an unfranked dividend, and you’ll get hit with a massive tax bill. We work with you to set up these structures properly from day one. It’s about building a “fortress” around your business that provides both flexibility and safety for the long haul.

How does being a company director affect my ability to get a home loan?

Being a company director can make getting a home loan slightly more complex because lenders like ANZ or NAB will usually want to see two years of company tax returns to verify your income. When you’re a sole trader, they just look at your personal tax return. As a director, they’ll look at the “serviceability” of the entire company. They want to see that the business is consistently profitable and that you aren’t just paying yourself a high wage while the company is drowning in debt. Most banks will “add back” certain non cash expenses like depreciation to your net profit, which can actually help you qualify for a larger loan than you might expect. They’re looking for stability and a track record of at least 24 months of solid trading history.

If you’ve only just switched from a sole trader to a company, some lenders might see you as a “new” business, even if you’ve been doing the same work for ten years. This is why it’s vital to keep your sole trader records and show a continuous line of income during the transition. Some specialized lenders are more flexible and might only require one year of company returns if you can show a strong history in the same industry. We often work directly with our clients’ mortgage brokers to provide the necessary financial statements and “letter of comfort” to explain the business’s performance. It’s all about presenting a professional and transparent picture of your financial health. With the right preparation and clean books, being a director shouldn’t stop you from getting your dream home; it might even help you if the company has significant retained earnings.

Related Posts

{kind=link}

{kind=link}

{kind=link}

{kind=link}