What Is a Sole Trader in Australia? A Complete Guide

If you’re starting a business or thinking about registering one, you’ve probably come across the term sole trader and wondered exactly what it means for you. What is a sole trader in Australia comes down to one simple idea: you and your business are legally the same entity. There’s no separate company structure, no shareholders, just you, trading under your own name or a registered business name, taking on all the legal and financial responsibility yourself.

This guide answers the question properly. We’ll cover how sole trader status works under Australian law, what it means for your tax obligations, and how it compares to running a company or partnership, so you can see whether it actually suits how you want to operate.

We’ve spent 25 years helping Melbourne business owners choose the right structure and stay compliant once they’ve picked it. This article draws on that experience to give you a practical, no-nonsense explanation of sole trader status, covering registration, ABNs, tax rates, and the point where switching structures starts to make financial sense.

Why the sole trader structure matters for your business

Most people default to the sole trader structure because it’s the path of least resistance. No registration fees with ASIC, no company constitution, no separate tax return for the business itself. You simply apply for an ABN, and if you’re trading under a name other than your own, register that business name too. For tradies, freelancers, consultants and small retailers just starting out, this simplicity is exactly what makes the structure work.

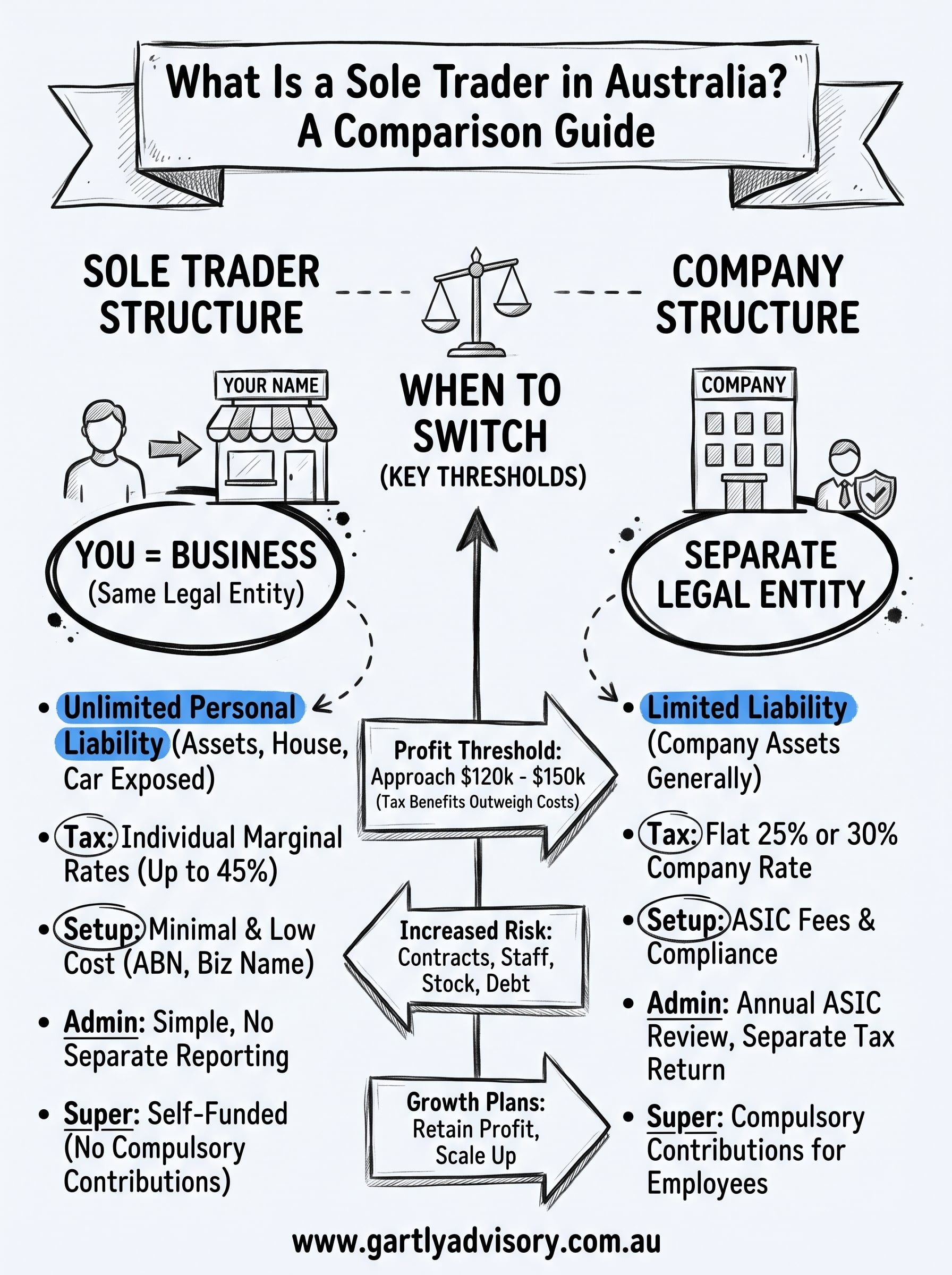

But the trade-off is significant, and it’s the part people underestimate. Because you and the business are the same legal entity, unlimited personal liability applies. If the business racks up debt, gets sued, or a client claims damages, your personal assets, your house, your car, your savings, are all fair game for creditors. A company structure puts a legal wall between the business and your personal wealth. As a sole trader, that wall doesn’t exist.

As a sole trader, there’s no legal separation between you and your business, so every debt and every risk lands squarely on your shoulders.

Tax treatment is the other piece that catches people out. Business income gets added straight to your personal income and taxed at individual marginal rates, which currently top out at 45% plus the Medicare levy for high earners, according to the Australian Taxation Office. Compare that to the flat 25% or 30% company tax rate, and you can see why growing sole traders often start asking questions about restructuring once profits climb past a certain point.

Here’s a quick snapshot of what’s at stake:

| Factor | Sole trader impact |

|---|---|

| Liability | Unlimited, personal assets exposed |

| Setup cost | Minimal, ABN and business name only |

| Tax rate | Individual marginal rates (up to 45%) |

| Ongoing admin | Low, no separate company reporting |

| Superannuation | Self-funded, no compulsory employer contributions |

Superannuation deserves a mention too. Nobody pays super for you when you’re a sole trader. Employees get compulsory contributions from their employer, but you’re on your own unless you set up voluntary payments. Combine that with the liability exposure and the tax curve, and you can see why understanding this structure properly, before you register, matters far more than most new business owners realise.

How to set up as a sole trader in Australia

Setting up as a sole trader is genuinely straightforward, which is part of the appeal. You don’t need a solicitor, a company constitution, or ASIC registration. What you do need is an Australian Business Number (ABN), which you can apply for free through the Australian Business Register. Once that’s approved, you’re legally trading.

The core steps

Most people get set up within a day or two if their details are in order. Here’s the practical sequence we walk clients through:

- Apply for an ABN through the Australian Business Register, using your tax file number.

- Register a business name with ASIC if you’re trading under anything other than your own legal name.

- Open a separate bank account for business transactions, even though it’s not a legal requirement.

- Register for GST if you expect turnover above $75,000 a year.

- Set up your record-keeping system before your first invoice goes out, not after.

Getting your ABN sorted is only step one. Solid record-keeping from day one is what actually keeps a sole trader out of trouble at tax time.

Getting the paperwork right from the start

Record-keeping trips up more sole traders than any other part of this structure. You’re required to keep receipts, invoices, and bank statements for five years, and the ATO can ask for them at any point. Many new sole traders underestimate how quickly this becomes messy without a system, particularly once they’re juggling multiple clients or projects. Setting up cloud accounting software from the outset, rather than retrofitting it after your first tax return, saves hours of reconstruction work and reduces the risk of missed deductions.

Sole trader vs company: which structure fits you

The decision between staying a sole trader and switching to a company structure usually comes down to three things: liability, tax, and growth plans. If you’re running a low-risk operation with modest profit, sole trader status often makes sense. But once you’re carrying stock, hiring staff, signing contracts with real exposure, or your profits push you into the top marginal tax brackets, a company structure starts looking a lot more attractive.

The right structure isn’t about which one sounds more professional, it’s about matching the setup to your actual risk and profit level.

Here’s how the two stack up on the factors that matter most:

| Factor | Sole trader | Company |

|---|---|---|

| Legal separation | None, you are the business | Separate legal entity |

| Liability | Unlimited, personal assets exposed | Limited to company assets (generally) |

| Tax rate | Individual marginal rates, up to 45% | Flat 25% or 30% company rate |

| Setup cost | Free to minimal | ASIC registration fees apply |

| Ongoing compliance | Minimal | Annual ASIC review, separate tax return |

| Profit retention | Not possible, all profit is yours | Can retain profit in the company |

When the switch actually pays off

We generally start the conversation with clients once taxable profit approaches $120,000 to $150,000 a year, because that’s roughly where the tax gap between individual and company rates becomes meaningful enough to offset the extra compliance cost. Below that threshold, the ASIC fees and accounting overhead of a company often outweigh the tax saving.

Moving structures isn’t something to decide alone with a spreadsheet. Get advice before you register the company, because restructuring after the fact, transferring assets, closing the sole trader ABN, can trigger tax consequences that a bit of forward planning avoids entirely.

Real-world examples of sole trader businesses

Across Melbourne, sole trader status shows up in almost every trade and service industry you can name. Tradies, hairdressers, personal trainers, freelance designers and small retail operators all tend to start here, because the paperwork is light and the income is immediate. Understanding what is a sole trader in Australia becomes a lot clearer once you see it in action across real businesses rather than just in legal definitions.

Common industries where sole trader status thrives

Here’s where we see this structure working well for clients, usually in the early stages of a business:

- Trades and construction: electricians, plumbers and carpenters working solo or with one apprentice

- Consulting and freelance services: bookkeepers, marketers, copywriters and IT contractors

- Personal services: hairdressers, tutors, massage therapists and personal trainers

- Small retail and online stores: market stallholders and Etsy or Shopify sellers turning over under $75,000

Each of these examples shares the same profile: low startup capital, manageable risk, and a single decision-maker.

When the numbers tell a different story

Growth changes the picture fast. A sole trader electrician who starts with one van and no staff might operate comfortably for years. But once he hires two apprentices, signs a $200,000 commercial contract, and starts carrying stock on account, the liability exposure and tax bracket both shift dramatically.

A business that suited sole trader status at $60,000 turnover often stops suiting it at $250,000, and the risk grows quietly in the background until something goes wrong.

Watching that transition point closely, rather than reacting after a bad year, is what separates businesses that scale smoothly from those that get caught out.

Finding the right fit for your venture

So, what is a sole trader in Australia? It’s the simplest legal structure available, but simple doesn’t mean risk-free. You get low setup costs and minimal admin, and in exchange you carry unlimited personal liability and pay tax at individual marginal rates rather than the flatter company rate. That trade-off works brilliantly for many businesses in their early years, and badly for others once turnover, staff, or contract risk grows.

The real skill isn’t choosing a structure once and forgetting about it. It’s reviewing that decision as your business changes, before a bad year forces the conversation. Profit thresholds shift, liability exposure grows quietly, and the right answer at $60,000 turnover isn’t always the right answer at $250,000.

If you’re weighing up sole trader status against a company structure, or you’re due for a proper review, talk to the team at Gartly Advisory and get advice built around your actual numbers, not a generic checklist.

{kind=link}

{kind=link}

{kind=link}

{kind=link}