Capital Gains Tax Discount Australia: How It Works & Who Qualifies

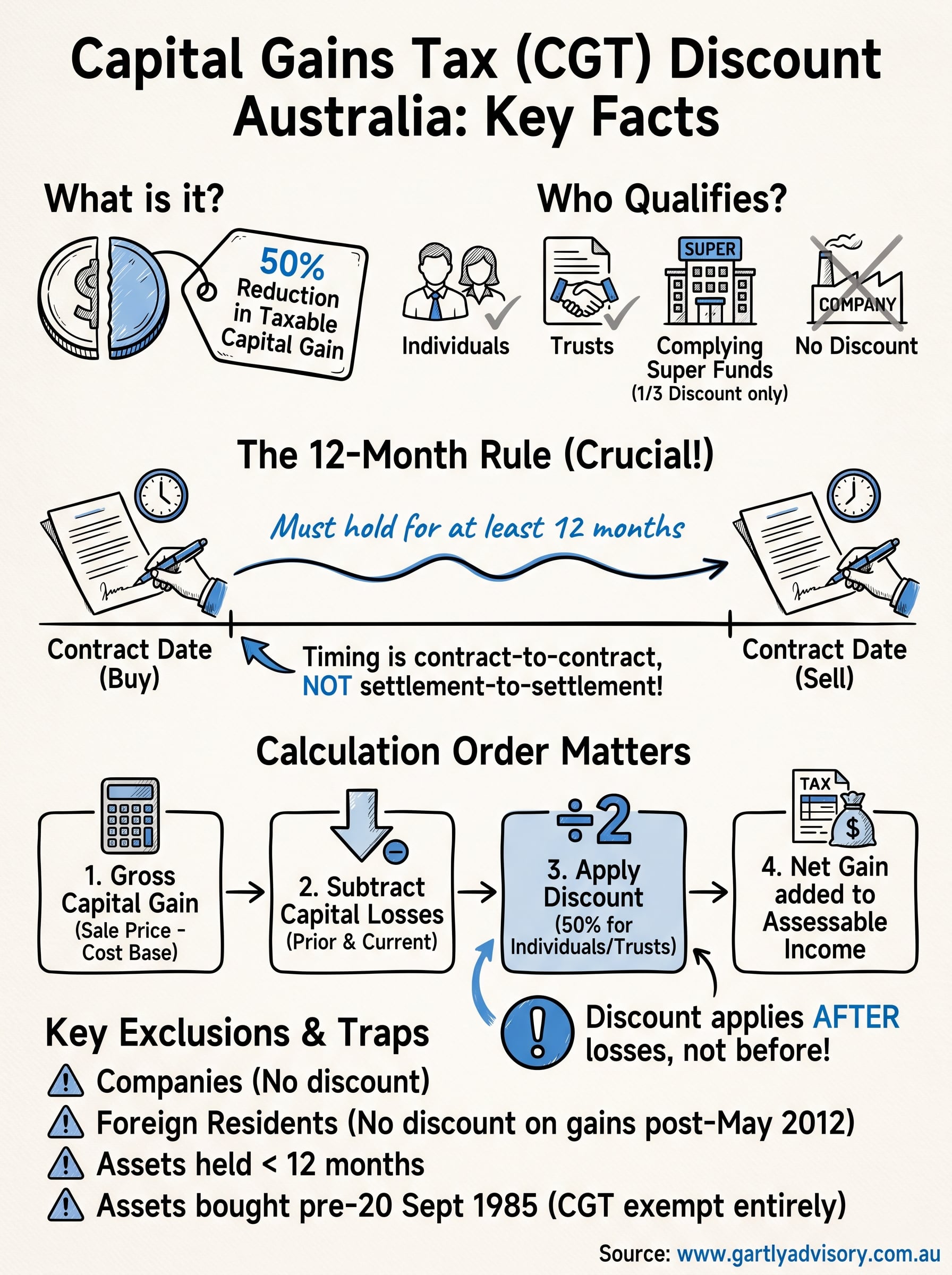

Sell an asset you’ve held for a while and the tax bill can come as a shock, until you realise you might only pay tax on half the gain. The capital gains tax discount australia rules allow individuals and trusts to cut their taxable capital gain by 50%, provided you’ve held the asset for at least 12 months before selling. It sounds simple, but the eligibility rules, the ordering rules with other concessions, and the entity type you hold the asset in all change the outcome.

This article walks through exactly how the 50% CGT discount applies, who actually qualifies (and who’s excluded, such as companies), and how it interacts with the small business CGT concessions many of our clients rely on when selling a business or investment property. We’ll also flag the proposed changes currently being debated in Canberra that could affect discount eligibility for higher-value assets.

We see this issue constantly with clients selling investment properties, business assets, or shares, often without realising how much the timing of a sale can change their tax outcome. Read on to understand where you stand before your next disposal.

Why the CGT discount matters for your tax bill

Most business owners we meet underestimate how much the CGT discount actually saves them until they see the numbers side by side. A capital gain sitting outside the discount gets added in full to your assessable income, taxed at your marginal rate, which can be as high as 45% plus the Medicare levy. Apply the discount and only half that gain counts, which for someone on the top marginal rate turns an effective tax rate on the gain from 47% down to roughly 23.5%. That difference isn’t academic. On a $400,000 gain from selling an investment property or a business, it can mean tens of thousands of dollars staying in your pocket rather than going to the ATO.

The discount changes your entire sale strategy

The 50% discount doesn’t just reduce a tax bill after the fact, it shapes decisions made months or years before a sale. Business owners weighing up whether to sell now or wait another few months to clear the 12-month holding period often find that patience alone is worth a five- or six-figure tax saving. We regularly advise clients to delay settlement, restructure a sale contract, or time an asset disposal around the end of a financial year specifically because of how the discount interacts with their income for that year.

Holding an asset those extra few months to qualify for the discount can be worth more than any other single tax decision you make that year.

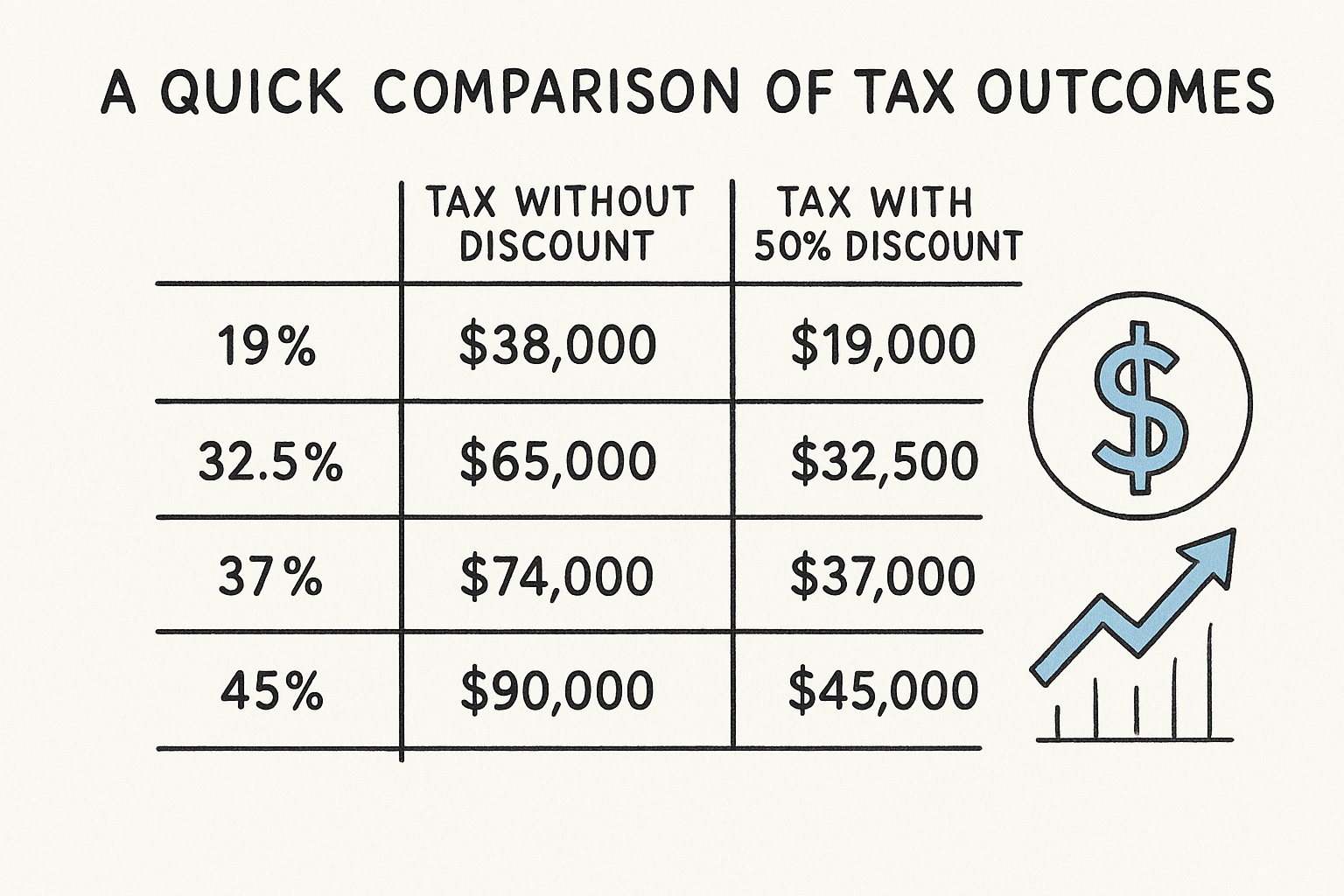

A quick comparison of tax outcomes

Seeing the discount applied against different marginal rates makes the impact obvious. The table below assumes a $200,000 capital gain and no other concessions applied.

| Marginal tax rate | Tax without discount | Tax with 50% discount | Tax saved |

|—|—|—|

| 19% | $38,000 | $19,000 | $19,000 |

| 32.5% | $65,000 | $32,500 | $32,500 |

| 37% | $74,000 | $37,000 | $37,000 |

| 45% | $90,000 | $45,000 | $45,000 |

Note: figures exclude the Medicare levy and any Medicare levy surcharge, which push the real saving even higher for most taxpayers.

It stacks with other concessions

Qualifying for the discount also opens the door to further reductions. Small business owners who meet the basic conditions for the small business CGT concessions can apply the 50% discount first, then layer the small business 50% reduction, the retirement exemption, or the 15-year exemption on top. Used correctly, some business owners selling an eligible active asset pay little to no tax on the sale at all. That’s a meaningful outcome for someone approaching retirement or an exit, and it’s exactly the kind of planning we work through with clients well before a sale goes to contract.

Getting this wrong, or missing the interaction between concessions, is one of the most common ways business owners overpay tax on a sale they only make once. The Australian Taxation Office sets out the mechanics of the discount and its ordering rules in detail on its own guidance pages, and it’s worth cross-checking your position there or with an adviser before you sign anything (see the ATO’s guidance on the CGT discount for the current rules).

How to qualify for and apply the 50% CGT discount

Qualifying for the 50% CGT discount isn’t automatic, and the ATO checks each condition before accepting a discounted gain on your tax return. You need to be an individual, trust, or complying super fund (companies are excluded entirely), you must have owned the asset for at least 12 months before the CGT event, and the asset can’t have been acquired under certain rollover concessions that reset the clock. Miss any one of these and you’re back to paying tax on the full gain.

The eligibility checklist

Before you assume the discount applies, run through this list. It’s the same sequence we work through with clients before any significant asset sale.

- Confirm the entity type: individuals, trusts and complying super funds qualify; companies do not

- Check the holding period runs to 12 months or more from the contract date of purchase to the contract date of sale, not settlement

- Rule out any exclusions, such as gains from assets acquired before 20 September 1985 or certain revenue assets

- Calculate the capital gain first, apply any capital losses, then apply the discount to what’s left

- Layer any small business CGT concessions after the discount, in the correct order set out by the ATO

Get the holding period wrong by even a week and you lose the entire discount, not just part of it.

Applying the discount on your tax return

Once you’ve confirmed eligibility, applying the discount is mechanical rather than discretionary. You work out the capital gain in full, offset any current or carried-forward capital losses against it, and only then halve what remains before it’s added to your assessable income. This ordering matters: losses reduce the gain before the discount applies, not after, so you can’t double up the benefit.

For trusts, the discount is applied at the trust level before distributable gains are streamed to beneficiaries, who then report their share on their own return. Super funds in accumulation phase get a reduced one-third discount instead of 50%, which trips up plenty of self-managed super fund trustees who assume the same rate applies across every entity. Getting the sequencing right, especially where multiple concessions stack together, is where a second set of eyes from your accountant earns its fee well before the contract of sale is signed.

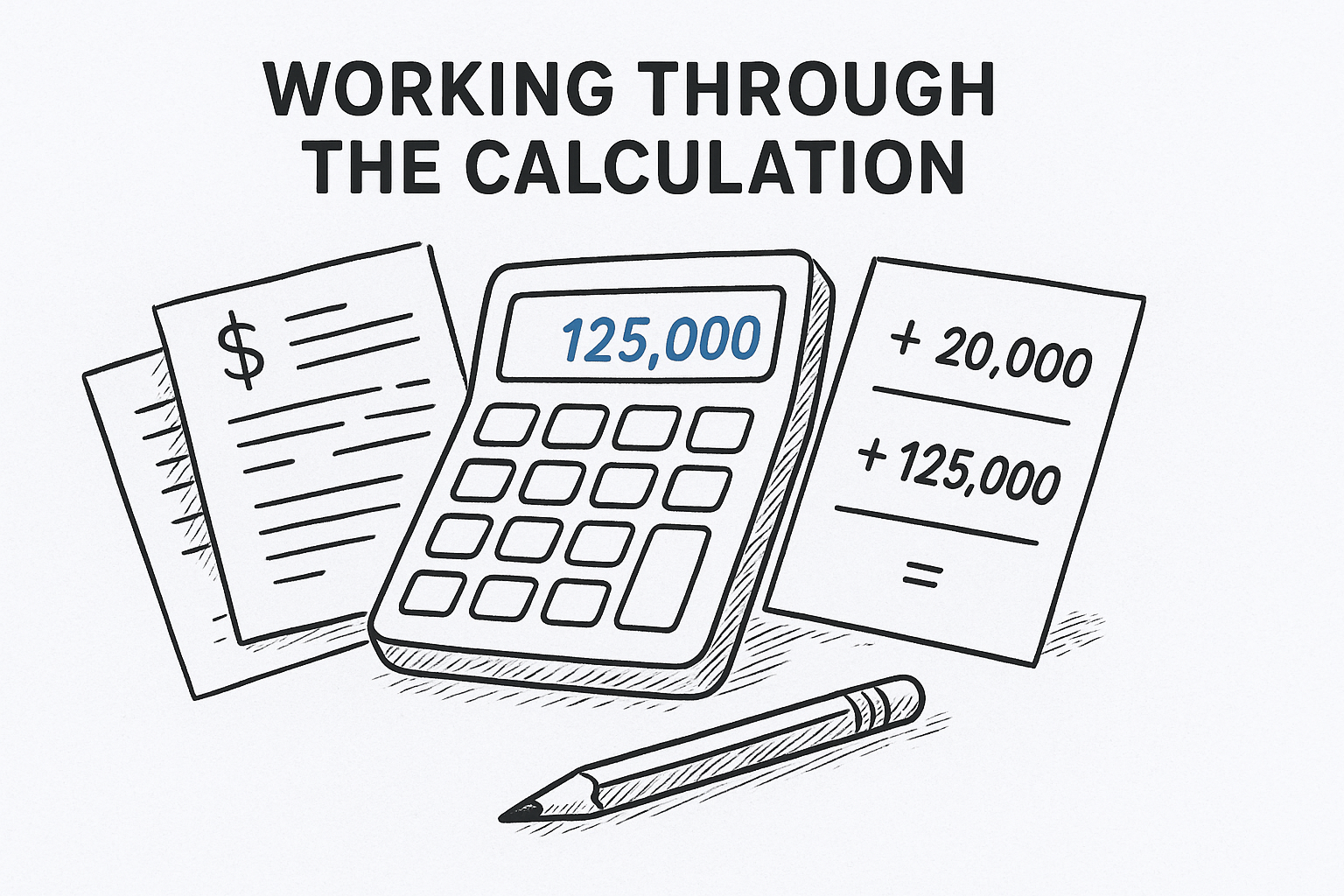

A worked example of the CGT discount in action

Numbers make this easier to follow than any explanation on its own, so let’s run a real scenario. Say you bought an investment property in Ormond for $650,000 in March 2021, and you sell it in June 2026 for $950,000. You’ve held it well past the 12-month threshold, so the 50% CGT discount is available, and you’ve got $18,000 in selling costs (agent fees, legal costs) plus $12,000 in capital improvements to add to your cost base.

Working through the calculation

Before applying any discount, you need the capital gain in full, calculated as sale price minus cost base. Here’s how that breaks down:

| Step | Amount |

|---|---|

| Sale price | $950,000 |

| Cost base (purchase + costs + improvements) | $680,000 |

| Capital gain before discount | $270,000 |

| Less: prior year capital loss carried forward | $20,000 |

| Net capital gain after losses | $250,000 |

| CGT discount (50%) | $125,000 |

| Discounted gain added to assessable income | $125,000 |

A $270,000 gain shrinks to a $125,000 tax bill impact once losses and the discount are correctly applied in order.

What that means for your tax bill

Assuming you’re on the top marginal rate of 45% plus the 2% Medicare levy, that $125,000 discounted gain adds roughly $58,750 to your tax liability for the year. Compare that to the $126,900 you’d owe if the full $270,000 gain (after losses) was taxed without any discount, and the saving from qualifying for the discount alone is over $68,000. That’s the difference between selling one month before the 12-month mark and one month after.

Ordering matters here too. Losses get applied to the raw gain first, then the discount halves what’s left, never the other way around. Skip that sequence and you understate your tax saving, or worse, you overstate it and end up with an ATO adjustment down the track. Reviewing the calculation with your accountant before lodging, particularly where losses, improvements, or multiple properties are involved, avoids a costly correction later. Property sales like this one are exactly where the gap between doing your own tax return and getting proper advice shows up in real dollars, not just peace of mind.

Upcoming changes to the CGT discount from 2027

Canberra has floated changes to the CGT discount for years, and momentum has been building again. Tax reform discussions currently circulating in federal policy circles include proposals to reduce the discount from 50% to 25% for higher-income earners or for gains above a certain threshold, with some versions targeting investment property specifically. Nothing has passed into law as at the date of this article, but the direction of travel matters if you’re planning a sale over the next few years. Treat any proposed change as a planning trigger, not a certainty, until it’s actually legislated.

What’s being proposed and why it matters

The rationale behind these proposals centres on housing affordability and revenue concerns, with successive reviews (including work referenced by Treasury) pointing to the discount as one of the larger concessions in the personal tax system by cost to revenue. Most versions of the proposal being discussed would not touch owner-occupied homes, and many carve out small business asset sales entirely, but investment properties and shares held by individuals are usually squarely in scope.

A halved discount on a large capital gain can double your tax bill overnight, so timing a sale around any confirmed law change is worth watching closely.

Why timing your sale now still matters

Selling before any change takes effect locks in the current 50% rate on that gain, which is a meaningful reason some clients are bringing forward settlement dates on investment properties they’d otherwise have held longer. Others are choosing to wait, betting that a change won’t survive the legislative process, as has happened with similar proposals in the past. Either bet carries risk, so this isn’t a decision to make on assumption alone.

How we’re advising clients to prepare

Until legislation actually passes, we treat these proposals as a reason to model both scenarios rather than a reason to panic-sell. That means:

- Running your numbers under the current 50% discount and under a reduced 25% scenario

- Checking whether your asset falls under any small business or owner-occupier carve-out being discussed

- Watching for draft legislation rather than reacting to media commentary alone

- Confirming the current legislated position directly through the Australian Treasury before making a final call

We’ll update our advice to clients as soon as anything moves from proposal to law.

Common mistakes that can cost you the CGT discount

Every year we see clients lose part or all of their CGT discount through avoidable errors, usually because the rules got applied in the wrong order or the holding period got miscounted. None of these mistakes are complicated once you know what to look for, but they’re expensive when they slip through unnoticed until tax time.

Getting the holding period wrong

Business owners often count from settlement date rather than contract date, which can push an asset just under the 12-month mark without them realising it. The ATO looks at the date you entered the contract to buy and the date you entered the contract to sell, not when the money actually changed hands. A property that settles 13 months after purchase but was contracted only 11 months after purchase doesn’t qualify, full stop.

Miscounting the holding period by even a few weeks can wipe out a discount worth tens of thousands of dollars.

Applying the discount before losses

Sequencing errors are just as common. Some taxpayers halve the gain first and then subtract losses, which overstates the benefit and creates a mismatch the ATO will query. Losses always reduce the raw gain first, and only the remainder gets discounted.

Other traps we see regularly

Beyond timing and sequencing, a handful of recurring mistakes cost clients real money each year:

- Assuming a company can access the discount (it can’t, ever)

- Forgetting that assets bought before 20 September 1985 sit outside the CGT regime entirely

- Overlooking that super funds in accumulation phase only get a one-third discount, not 50%

- Missing the correct order when stacking the discount with small business CGT concessions

- Failing to keep records proving the contract date, especially for off-the-plan property purchases

Catching these issues before you lodge, rather than after, is where a proper review pays for itself. If you’re unsure which of these applies to your situation, it’s worth running your numbers past an adviser before the contract of sale is even signed, not after settlement when your options have narrowed considerably.

CGT discount rules for trusts, super funds and foreign residents

The 50% discount doesn’t apply the same way across every entity type, and this is where a lot of confusion sets in for clients running a family trust or a self-managed super fund alongside their personal investments. Trusts, complying super funds and individuals each sit under different rules, and foreign residents face restrictions that catch plenty of expats off guard when they eventually sell an Australian asset.

Trusts and streaming the discount

A discretionary or family trust applies the discount at the trust level before any distribution decision is made, then streams the discounted gain out to beneficiaries who report their share on their own tax return. Beneficiaries can’t apply a further discount on top of what’s already been applied inside the trust, and the trustee needs to make a valid distribution resolution before 30 June for the streaming to hold up under ATO scrutiny. Get the resolution wrong or lodge it late, and the gain can end up taxed to the trustee at the top rate instead of flowing through to beneficiaries at their own marginal rates.

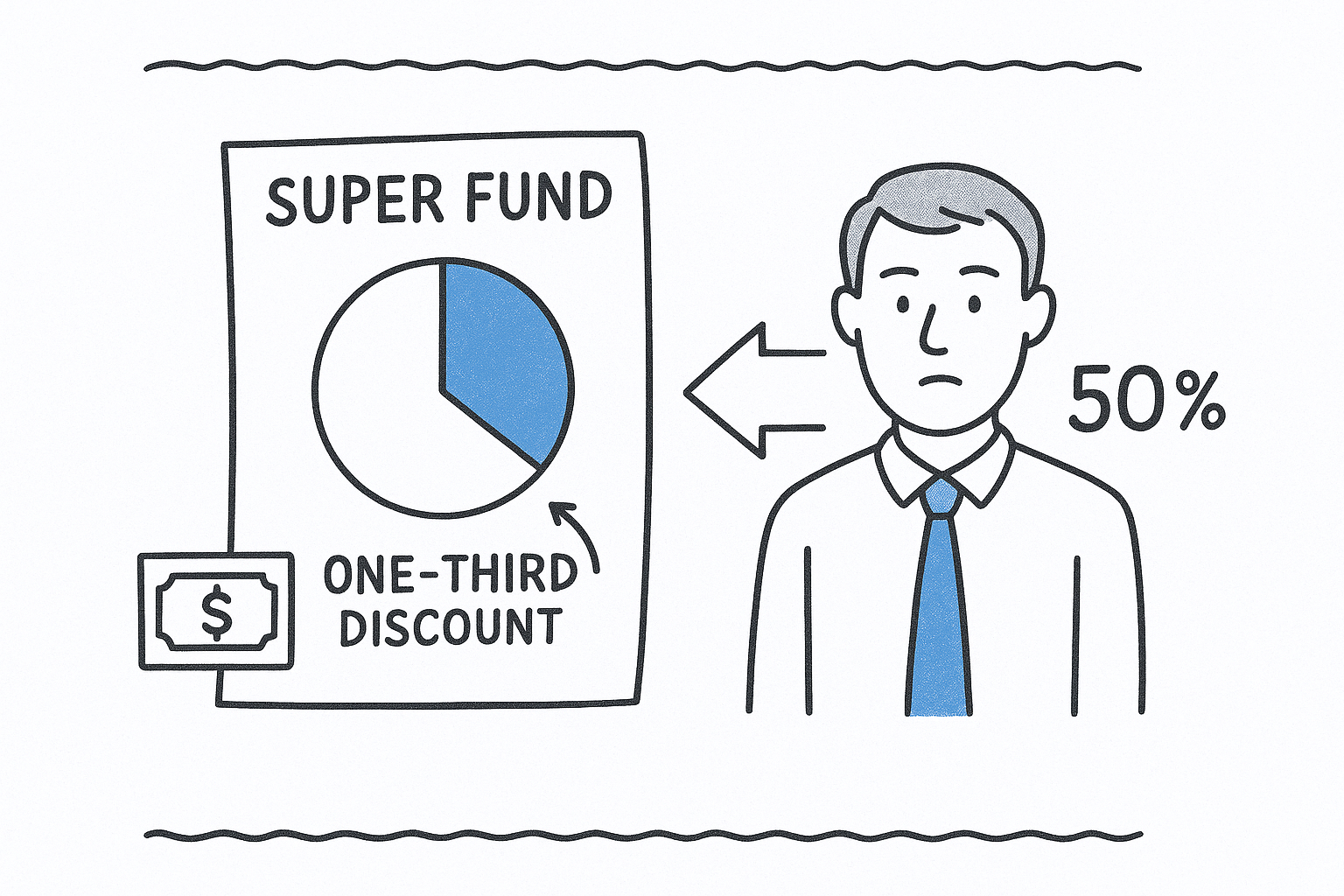

Super funds get a smaller discount

Complying super funds in accumulation phase only receive a one-third discount, not 50%, which is a common trip-up for SMSF trustees comparing their fund’s outcome to a personal investment. Funds fully in pension phase may pay no tax at all on the gain, depending on the members’ balances and the pension arrangements in place. Table below sets out the different treatment side by side:

| Entity type | Discount available |

|---|---|

| Individual | 50% |

| Trust (streamed to individual beneficiary) | 50% |

| Complying super fund (accumulation) | One-third |

| Complying super fund (pension phase) | Often nil tax |

| Company | No discount |

A self-managed super fund in accumulation phase pays tax on two-thirds of a gain, not half, so don’t assume the personal rate carries across.

Foreign residents lose the discount entirely

Foreign residents and temporary residents haven’t been able to claim the CGT discount on gains accrued since 8 May 2012, regardless of how long they’ve held the asset. If you’ve spent part of the ownership period as an Australian resident and part as a foreign resident, the gain gets apportioned, with only the resident-period share eligible for any discount at all. This catches out plenty of Australians who move overseas for work and later sell a property back home, so it’s worth confirming your residency status for tax purposes well before signing a contract of sale (see the ATO’s guidance for foreign and temporary residents for the current apportionment rules).

Planning ahead with the CGT discount

Getting the capital gains tax discount australia rules right comes down to three things: knowing your entity type, tracking the correct holding period from contract date, and applying losses before the discount, not after. Get the sequencing wrong and you either overpay or trigger an ATO adjustment later. Get it right, and you keep tens of thousands of dollars that would otherwise go straight to tax.

Proposed changes to the discount are still just proposals, but they’re worth watching if you’re planning a sale over the next couple of years. Whether you’re selling an investment property, exiting a business, or restructuring assets inside a trust or SMSF, the right time to check your position is before the contract is signed, not after settlement.

If you want that certainty before your next sale, talk to the team at Gartly Advisory and get your numbers checked properly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}