Understanding Profit and Loss Statements: A Guide for Melbourne and Sydney Business Owners

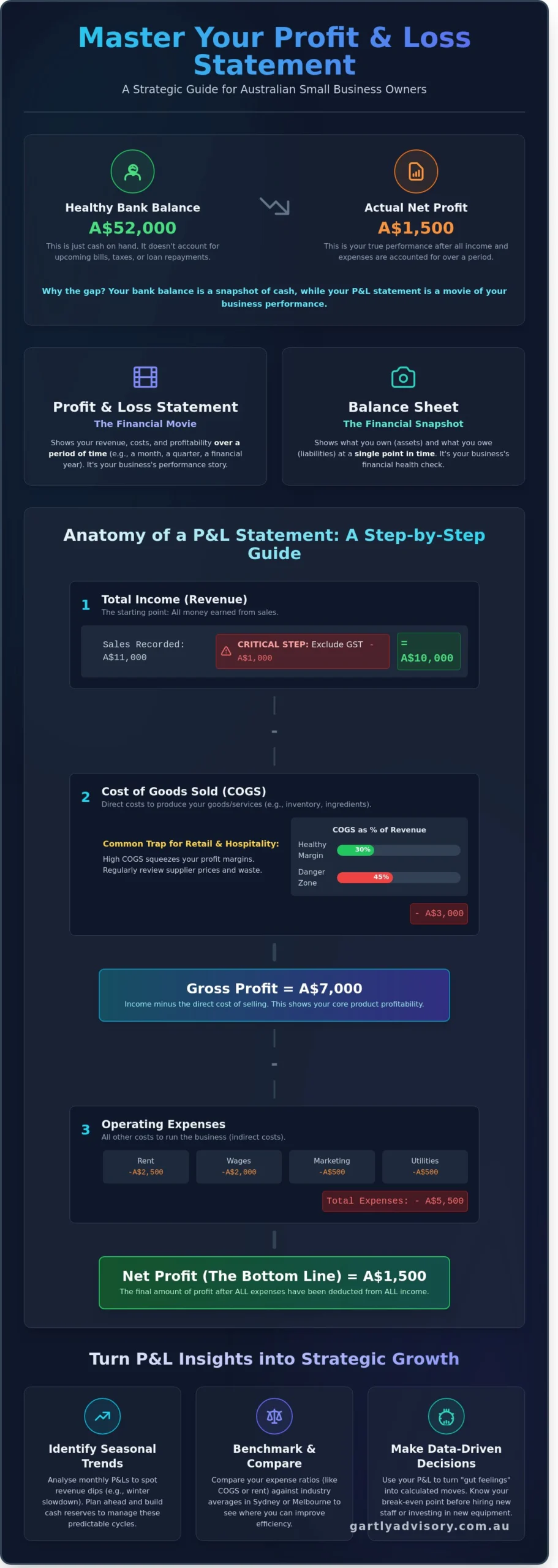

Why does your business bank account show a healthy balance when your tax return suggests you’re barely breaking even?

If you’ve ever felt blind to your true profitability or confused by the gap between cash flow and net profit, you aren’t alone. Many small business owners in Melbourne and Sydney find themselves trapped in this cycle of financial uncertainty. Truly understanding profit and loss statements is the first step to reclaiming your confidence and ensuring you’re ready for every GST obligation. It’s about moving beyond the numbers to see the real story of your business’s health.

Let’s unpack the basics of your P&L so you can spot financial red flags before they become crises. You’ll gain total control over your finances and learn how to drive growth in the competitive Australian market. We’ll explore the essential components of your statement, explain how to distinguish between profit and cash, and provide actionable tips to help you stay compliant with the ATO. By the end, you’ll have a clear map of exactly where your money is going and the data you need to scale with certainty.

Key Takeaways

-

Learn why your bank balance isn’t the true measure of success and how to view your P&L as a "financial movie" of your business performance.

-

Navigate the "Total Income" line with confidence by understanding what to exclude—like GST—to ensure your financial reporting remains accurate.

-

Avoid common "Cost of Goods Sold" traps that impact hospitality and retail sectors, helping you maintain healthier profit margins throughout the financial year.

-

Master understanding profit and loss statements to move beyond basic compliance and gain the financial control needed to drive strategic growth in 2026.

-

Discover how to use trend analysis and local benchmarking to compare your performance against other Sydney and Melbourne businesses and spot seasonal dips early.

Table of Contents

-

Demystifying the Profit and Loss Statement for Australian Business Owners

-

A Step-by-Step Guide to Reading Your Statement in Melbourne and Sydney

Demystifying the Profit and Loss Statement for Australian Business Owners

Think of your business as a feature film. While other reports might give you a still photo, the Profit and Loss (P&L) statement is the financial movie of your performance over a specific period. For the 2.5 million small businesses operating across Australia, the bank balance is often the first thing checked in the morning. However, many owners in Sydney and Melbourne fall into a dangerous trap, mistaking a healthy bank account balance for actual profit. Data from the Australian Bureau of Statistics indicates that over 60% of small businesses fail within their first three years, often because they lack a clear view of their margins.

A P&L statement is a summary of revenue, costs, and expenses incurred during a specific period, such as a month or financial year. Its primary purpose is to track every dollar coming in against every cent going out. This process reveals your bottom line, showing whether you are truly making money or just moving it around. If you plan to scale or eventually exit, a clean P&L is essential. In the competitive Gold Coast market, for example, potential buyers and lenders look for at least three years of consistent P&L data to verify business value. Without it, you lack the evidence needed to build professional trust.

Pro Tip: Don’t wait for your accountant to send you a year-end report. Set up a monthly review in your cloud accounting software to catch small leaks in your cash flow before they become floods.

The Difference Between a P&L and a Balance Sheet

It helps to view these documents through a simple analogy. The P&L is your speedometer, showing how fast you are moving and how much energy you are using right now. The Balance Sheet is your fuel gauge, showing how much is left in the tank. While the Balance Sheet provides a snapshot of what you own and what you owe at a single point in time, the P&L tells the story of your journey between two dates. To get a comprehensive view of your business health, you need to read both together. You can learn more about the technical structure of what an income statement is to see how these categories are traditionally organised, but the focus for an Australian SME is always on the narrative the numbers tell about daily operations.

Why "Understanding Profit and Loss" is Your Secret Growth Weapon

Mastering the art of understanding profit and loss statements shifts your role from a reactive manager to a proactive strategist. It moves you beyond basic tax compliance and into the space of genuine business advisory. When you dive into the data, you can identify which specific services or products are actually paying the bills in your local area. You might discover that a high-volume product in your Sydney warehouse actually has a lower profit margin than a niche service you offer in Melbourne once you factor in rising logistics costs.

-

Identify seasonal trends where revenue dips so you can plan cash reserves.

-

Compare your current expenses against the previous financial year to spot "subscription creep."

-

Calculate your break-even point to know exactly how much you need to sell each week to stay afloat.

By regularly understanding profit and loss statements, you gain the confidence to make big decisions. Whether it’s hiring a new team member in Brisbane or investing in a new storefront in Parramatta, your P&L provides the evidence you need to move forward safely. It turns "gut feelings" into calculated moves that support your long-term dreams.

A Step-by-Step Guide to Reading Your Statement in Melbourne and Sydney

When you sit down to review your financial reports, the first figure you’ll see is "Total Income" or "Revenue". It’s easy to get excited by a large number here, but you need to look closer. For Australian businesses, this top line must exclude GST. If your Melbourne boutique recorded A$11,000 in sales this week, your P&L should only show A$10,000 as income. The remaining A$1,000 belongs to the ATO, not your business. Correctly understanding profit and loss statements starts with recognising that your top line isn’t your spending money; it’s the raw starting point before the reality of costs sets in.

Retailers and hospitality owners in Sydney often fall into the "Cost of Goods Sold" (COGS) trap. This section tracks the direct costs of producing your products, such as ingredients for a Surry Hills cafe or inventory for a Richmond clothing store. If your COGS is sitting at 45% of your revenue when the industry average is 30%, your margins are being squeezed by waste or rising supplier prices. We often see businesses struggle because they don’t update these costs frequently enough. In 2024, supplier prices in Australia have fluctuated by up to 12% in some sectors, making weekly tracking vital for survival.

Operating expenses are the next hurdle. You can split these into fixed and variable costs. Your rent for a Bayside Melbourne office is a fixed cost; it stays the same regardless of your monthly sales. Variable costs, such as digital marketing or casual wages, vary based on your activity. If your fixed costs exceed 40% of your total revenue, your business might lack the flexibility to survive a quiet month. Keeping a lean overhead is a hallmark of the most resilient Victorian and NSW enterprises we support.

Finally, we reach the "Net Profit" or the bottom line. It’s a common misconception that this figure represents the cash you can take home. Net profit is what remains after all business expenses are paid, but before you pay yourself "drawings" or settle your income tax bill. If your P&L shows a A$50,000 profit, you still need to set aside roughly 25% to 30% for tax obligations depending on your structure. Understanding this distinction prevents the "tax time shock" that many unprepared owners face in July.

Cash vs. Accrual Accounting: Which One Are You Using?

Your P&L might show a healthy profit even if your bank account is empty. This usually happens because you’re using the accrual method. Accrual accounting records income when you send the invoice, not when the client pays it. This provides a more accurate long-term view of your small business accounting health, but it can mask immediate cash flow issues. Using Xero accounting allows you to toggle between cash and accrual views with one click, giving you the clarity needed to manage daily expenses while planning for future growth.

Local Considerations: GST, Payroll Tax, and Superannuation

To avoid overestimating your wealth, ensure every figure on your statement is "net" of GST. You should also watch your "Superannuation Payable" line closely. As of July 1, 2024, the Super Guarantee rate is 11.5%. If this liability is growing on your balance sheet but isn’t reflected as a paid expense on your P&L, you are falling behind. Consistency is key here. You should always verify that your internal reports align with the records held by your tax agent to ensure your BAS and annual returns are seamless. If these numbers feel overwhelming, you might find it helpful to speak with a specialist advisor who can help clarify your specific obligations.

Using Your P&L to Drive Strategic Growth in 2026

By the time 2026 arrives, successful business owners won’t just look at their bottom line once a year. They’ll use their financial data to make moves before their competitors even wake up. Truly understanding profit and loss statements means you can spot a 12% dip in Melbourne’s winter retail trade and adjust your stock orders before cash flow gets tight. If you’re running a professional services firm in Sydney or a hospitality venue on the Gold Coast, comparing your 18% net profit margin against the industry standard of 15% tells you exactly where you stand in the market.

Strategic growth requires a sharp eye for "Expense Creep." This happens when small costs, like a A$50 monthly software subscription or a 5% increase in utility rates, slowly erode your margins. Over a year, these minor leaks can drain A$10,000 or more from a typical SME. If you’re planning a successful exit or a franchise expansion in the next 24 months, your P&L must demonstrate clean, consistent profitability that a buyer can trust.

-

Trend Analysis: Compare your July 2025 figures to July 2026 to see if your growth is real or just a seasonal spike.

-

Benchmarking: Use local data to ensure your Sydney rent-to-revenue ratio stays below the dangerous 20% threshold.

-

Exit Readiness: Keep your personal expenses separate to show a "normalised" profit that attracts high-value investors.

Spotting Opportunities Beyond the Numbers

Your P&L acts as a green light for expansion. If your reports show that your current team in Ormond or Sydney is generating A$250,000 in revenue per head, it might be the perfect time to hire. This data-driven approach removes the guesswork from recruitment. These insights form the backbone of your business advisory Melbourne sessions, where we turn raw data into a roadmap for the future.

Practical Tip: Set a "Profit Target" of A$200,000 instead of just a "Revenue Target" of A$1.5 million. Revenue is a vanity metric; profit is what keeps your doors open and pays for your lifestyle.

Partnering with a Chartered Accountant for Deeper Insight

DIY accounting software is great for recording transactions, but it won’t tell you why your margins dropped by 4% last quarter. Partnering with a specialist provides a level of clarity that software alone cannot reach. At Gartly Advisory, we provide guidance that goes beyond simple tax compliance by looking at the story behind the spreadsheets. A proactive accountant helps you see around corners by interpreting P&L trends to anticipate market shifts before they impact your bank balance. We’ve spent 25 years helping Australians move beyond the numbers to build businesses that last.

Take Control of Your Business Future Today

Mastering the art of understanding profit and loss statements isn’t just about keeping the tax office happy. It’s about gaining the clarity you need to scale your Melbourne or Sydney business with confidence. By tracking your gross margins and overheads monthly, you’ll spot trends before they become problems. This proactive approach allows you to plan for 2026 with real data instead of guesswork. You’ve worked hard to build your dream, so don’t let complex numbers hold you back from the next level of growth.

At Gartly Advisory, we bring 35+ years of experience as Chartered Accountants who look beyond the numbers to provide genuine strategic support. Our team has earned 70+ 5-star Google reviews by helping business owners like you find hidden opportunities for profit. We’re here to simplify the complex and help you make informed decisions that stick. Let us be your trusted partner on your journey; book a consultation with Gartly Advisory today.

We’re excited to help you turn your financial data into a powerful tool for long term success. Let’s get started on your path to better business health together.

Frequently Asked Questions

Is a profit and loss statement the same as an income statement?

Yes, a profit and loss statement is exactly the same as an income statement. Both documents summarise your revenues, costs, and expenses over a specific period, such as a quarter or the 2024 financial year. In Australia, most accounting platforms use these terms interchangeably. Understanding profit and loss statements is vital because it reveals your net profit, showing if your Melbourne or Sydney business is truly sustainable after you’ve accounted for every expense.

Why does my P&L show a profit when I have no cash in the bank?

Profit doesn’t always equal cash because of how accrual accounting functions. Your P&L records a sale the moment you send an invoice, even if that A$4,500 payment hasn’t hit your account yet. You might also have spent cash on items that don’t appear as expenses, like repaying the principal on a A$30,000 bank loan. These cash outflows affect your bank balance but won’t reduce the profit figure shown on your statement.

How often should a small business owner in Australia review their P&L?

You should review your P&L statement at least once every 30 days. Waiting until the end of the Australian financial year on June 30 means you’re looking at historical data that’s often too old to act on. Regular monthly check-ins allow you to identify a 10% increase in supplier costs or a sudden drop in margins immediately. This proactive habit ensures you’re navigating your business journey with clear, current financial guidance rather than just guessing.

Can I use my P&L statement to apply for a business loan in Victoria or NSW?

Yes, lenders in Victoria and NSW require your P&L statements to evaluate any business loan application. Most Australian banks will request 24 months of financial records to confirm your business has the capacity to repay a new facility. Whether you’re seeking a A$100,000 expansion loan or a smaller line of credit, presenting professional and accurate statements builds the trust needed to secure approval. It proves your business is a stable and reliable investment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}