How to Set Up a Company Structure in Australia

Choosing the wrong structure at the start of your business costs Australian owners thousands of dollars in tax, admin, and legal headaches down the track. If you’re asking how to set up a company structure, you’re probably weighing up whether to trade as a sole trader, form a partnership, register a company, or set up a trust, and the honest answer is that it depends on your income, your asset protection needs, and where you plan to take the business over the next five years.

This guide walks you through each structure available in Australia, what it actually means for your tax bill and personal liability, and the practical steps to register it correctly with ASIC and the ATO. We’ll cover the situations where a company makes sense, when a trust offers better succession planning, and why many growing businesses end up using a combination of structures rather than just one.

We’ve helped hundreds of Melbourne business owners get this decision right the first time, and we’ll show you the same framework we use with clients: matching your structure to your actual growth plans, not just today’s turnover, so you’re not restructuring in two years’ time.

Why your business structure matters

Getting your business structure right from day one isn’t just paperwork. It determines who can come after your house if the business fails, how much tax you pay on every dollar you earn, and how easily you can bring in a partner, sell up, or hand the business to your kids later. Owners who treat this as a box-ticking exercise usually end up paying an accountant to unwind it a few years later, and that restructure often costs more than getting proper advice upfront would have.

Liability protection is the first thing to get right

As a sole trader, there’s no legal separation between you and your business. If a client sues you or a supplier chases an unpaid debt, your personal assets, including your house and savings, are on the line. A company structure creates a separate legal entity, so in most cases your liability is limited to what you’ve invested in the business. Trusts and partnerships sit somewhere in between, depending on how they’re set up, which is why matching structure to risk matters before you sign your first contract.

The structure you choose today decides whose assets are exposed if your business gets sued tomorrow.

Tax treatment changes your actual take-home

Different structures are taxed in completely different ways. Companies pay a flat company tax rate (25% for base rate entities, 30% otherwise, according to the Australian Taxation Office), while sole traders and partners pay tax at their individual marginal rate, which climbs steeply once profits grow. Trusts let you distribute income to beneficiaries in lower tax brackets, which can save real money for family businesses. Get this wrong and you could be handing thousands of extra dollars to the tax office every single year for no good reason.

Growth plans should shape your decision now, not later

How you plan to grow, bring in investors, or eventually sell matters just as much as your current turnover. Investors and banks generally prefer lending to or buying into companies rather than sole traders. Succession planning, particularly for family businesses, usually works better through a trust or a company with defined shareholding. Ignoring these future scenarios when you first register your structure is the single biggest reason business owners end up paying for a costly restructure down the track.

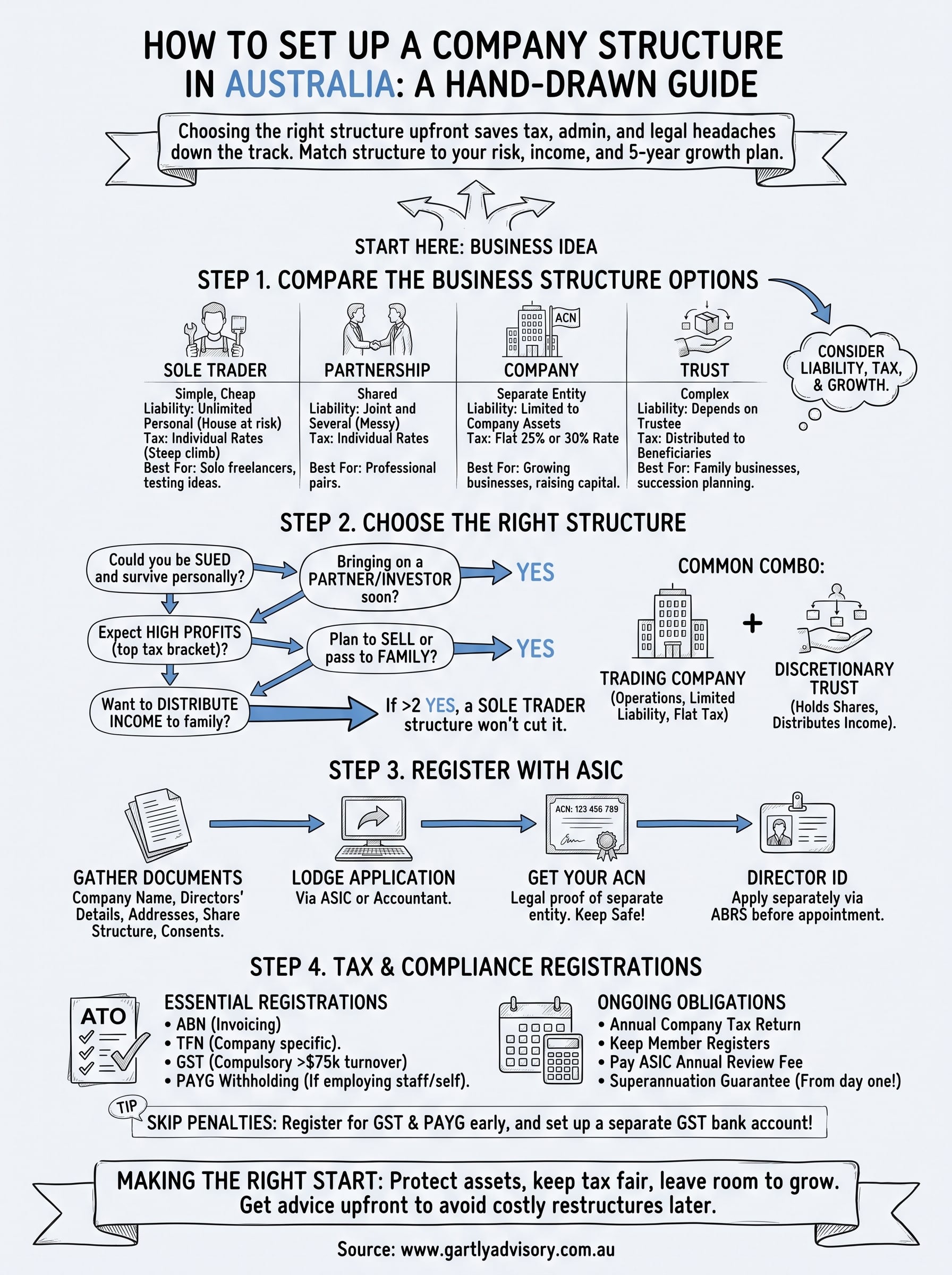

Step 1. Compare the business structure options

Before you touch any ASIC paperwork, lay out the four main options side by side. Sole trader is the simplest and cheapest to run, but it offers no asset protection. A partnership splits income and liability between two or more people, which works for professional pairs but gets messy fast if the relationship sours. A company gives you a separate legal entity, limited liability, and access to the flat company tax rate, at the cost of more reporting and ASIC fees. A trust distributes income to beneficiaries and protects assets well, but it’s more expensive to establish and needs a trustee, whether that’s you personally or a company you set up for the job.

The four core structures

| Structure | Setup cost | Liability | Tax treatment | Best for |

|---|---|---|---|---|

| Sole trader | Low | Unlimited personal liability | Individual marginal rates | Solo freelancers, testing an idea |

| Partnership | Low-medium | Joint and several liability | Individual marginal rates | Two or more professionals sharing a practice |

| Company | Medium | Limited to company assets | Flat 25% or 30% | Growing businesses, raising capital |

| Trust | Medium-high | Depends on trustee type | Distributed to beneficiaries | Family businesses, succession planning |

No single structure suits every business, so compare all four against your actual risk and growth plans before you pick one.

Reading the table against your situation

Match each row against where your business actually sits today, not where you hope it lands eventually. A tradie working alone with modest turnover rarely needs a trust from day one, while a business bringing on a co-founder and chasing investment usually outgrows sole trader status within the first year.

Step 2. Choose the right structure for your business

Once you’ve compared the options, the real work starts: matching a structure to your business, not the other way around. Most owners get this decision right by asking a handful of concrete questions rather than guessing based on what a mate down the pub set up for his business. Start with your risk exposure, then work through tax, ownership, and where you expect to be in three to five years.

Ask yourself these five questions

- Could a client, supplier, or employee reasonably sue you, and would you survive that personally?

- Are you bringing on a business partner, investor, or co-founder in the next 12 months?

- Do you expect profits to push you into the top individual tax brackets this year?

- Will you eventually want to sell the business, pass it to family, or wind it down cleanly?

- Do you have other income or family members you’d want to distribute business profits to?

If you answer yes to more than two of these, a sole trader structure probably won’t cut it for long.

Common structure combinations that work

Many established businesses in Melbourne don’t run on a single structure at all. A common setup pairs a trading company for day-to-day operations, limiting liability and locking in the flat tax rate, with a discretionary trust that owns the shares, giving you flexibility to distribute profits to family members in lower tax brackets. Trades businesses and franchise owners we work with often use exactly this combination once turnover passes six figures, because it protects the operating assets while still allowing income splitting at tax time.

Step 3. Register your company with ASIC

Once you’ve settled on a company structure, the actual registration happens through the Australian Securities and Investments Commission (ASIC), either directly or through a registered agent like your accountant. Registering a company gives it an Australian Company Number (ACN) and legal existence separate from you personally, which is the whole point of choosing this structure in the first place. Most owners can complete this within a few business days once the paperwork is in order.

Gather what you need before you apply

Sort your documentation before you start the ASIC application, because gaps here are what slow the process down. You’ll need:

- A proposed company name (or you can trade under your ACN)

- Full names, addresses, and dates of birth for all directors and shareholders

- The registered office address and principal place of business

- Details of share structure and who holds what percentage

- Each director’s consent to act, in writing

Lodge your application and get your ACN

Submitting the application through the ASIC portal or via your accountant triggers a review, and you’ll receive your ACN and certificate of registration once approved. Directors also need a director identification number (director ID) before they’re appointed, which you apply for separately through the Australian Business Registry Services.

Your ACN isn’t just a formality, it’s the legal proof that your business is now a separate entity from you.

Keep your certificate of registration somewhere safe. Banks, suppliers, and landlords will all ask for it when you open accounts or sign leases under the new company name.

Step 4. Complete your tax and compliance registrations

Getting your ACN doesn’t mean you’re ready to trade. You still need to register with the Australian Taxation Office (ATO) for the tax obligations that actually apply to your company, and skipping this step is why some new businesses end up with penalty notices in their first year instead of a smooth start.

Register for the essentials

Work through these registrations before you issue your first invoice:

- Australian Business Number (ABN): required for invoicing, claiming GST credits, and dealing with suppliers.

- Tax File Number (TFN): your company needs its own TFN, separate from your personal one.

- Goods and Services Tax (GST): compulsory once turnover exceeds $75,000, according to the ATO, optional below that threshold.

- PAYG withholding: needed the moment you employ staff, including yourself as a director drawing wages.

Skipping GST or PAYG registration doesn’t delay the obligation, it just delays the penalty notice.

Set up ongoing compliance from the start

Beyond the initial registrations, your company now carries ongoing obligations you didn’t have as a sole trader. You’ll lodge an annual company tax return, keep a register of members and officeholders, and pay ASIC’s annual review fee to keep your ACN active. Superannuation guarantee obligations kick in immediately for any employees, director included, so build this into your cash flow from month one rather than scrambling at quarter end. Most owners we work with set up a separate GST bank account straight away, because underestimating quarterly BAS liabilities is one of the fastest ways a growing business runs into a cash flow crunch.

Making the right start for your business

Getting your business structure right from the outset saves you years of unnecessary tax and the cost of a messy restructure later. Whether you land on a sole trader setup, a company, a trust, or a combination of the two, the goal is the same: protect your assets, keep your tax bill fair, and leave room to grow without starting over. The steps in this guide, comparing your options, matching them to your actual risk and growth plans, then registering correctly with ASIC and the ATO, give you a solid foundation to build on.

No two businesses face identical circumstances, though, and getting the fine detail wrong on tax or liability can be an expensive mistake to fix. If you want a second set of eyes on your situation before you register anything, talk to the team at Gartly Advisory and get it right the first time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}