How Does Negative Gearing Work? A Step-by-Step Breakdown

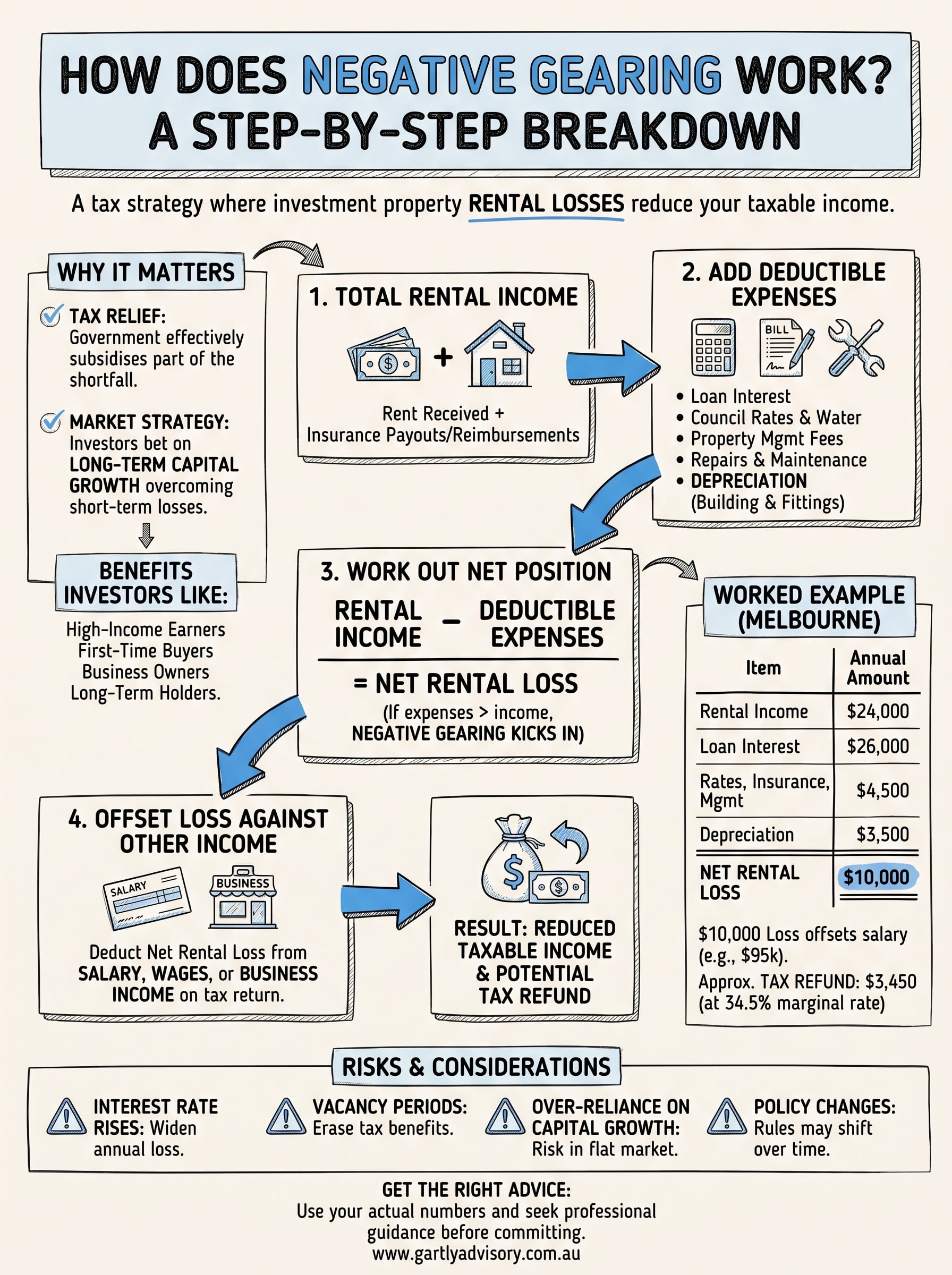

If you own an investment property that costs you more to hold than it earns in rent, you have probably heard the term thrown around at a barbecue without ever getting a proper explanation. How does negative gearing work in practice? At its core, it is a tax strategy where your rental losses reduce your taxable income, meaning the tax office effectively subsidises part of the shortfall. It sounds simple until you try to calculate it against your own numbers.

The mechanics involve more than just "losing money on purpose". You need to understand how loan interest, depreciation, and running costs stack up against rental income, and how that net loss gets applied against your salary or business earnings at tax time. Get the calculation wrong and you either overpay tax or invite an ATO review.

In this breakdown, we walk through the process step by step, from calculating your rental loss to claiming it correctly on your return. We have spent 35 years helping Melbourne property investors get this right, so we will also flag the common mistakes that turn a smart strategy into an expensive one.

Why negative gearing matters to property investors

Negative gearing matters because it changes the maths on almost every investment property purchase in Australia. When your rental losses offset other income, you are effectively getting the government to pick up part of the tab while you wait for the property to grow in value. For a lot of investors, that tax relief is the difference between an investment they can afford to hold and one that drains the household budget every month. It is not a loophole, it is baked into how the tax system treats investment income and expenses, and it has shaped the Australian property market for decades.

Negative gearing works because the tax office effectively shares the cost of your short-term loss in exchange for you taking on the long-term risk.

The scale of negative gearing in Australia

Australian Taxation Office data consistently shows that well over half of all rental property owners report a net rental loss in any given year. That is not a coincidence. Investors buy property expecting capital growth to outweigh the annual cash shortfall, and the tax deduction softens that shortfall while they wait. According to the Australian Taxation Office, rental deductions claimed each year run into the tens of billions of dollars, which tells you how embedded this strategy is in property investment decisions across the country.

Why it appeals to different types of investors

Negative gearing does not appeal to everyone for the same reason. Here is how it typically plays out across different investor profiles:

- High-income earners use it to reduce their marginal tax rate exposure while building a property portfolio.

- First-time investors rely on it to make an otherwise unaffordable mortgage repayment manageable.

- Business owners often combine it with other structures, such as trusts, to manage overall tax outcomes across multiple income streams.

- Long-term holders treat the tax deduction as a bridge, banking on rent increases and capital growth to eventually turn the property cash flow positive.

Business owners in particular need to be careful here. If you are already claiming deductions through a company or trust structure, layering a negatively geared property on top without proper advice can create timing mismatches or trigger unexpected tax bills. Considering how it interacts with your overall financial strategy, rather than treating it as a standalone decision, is where a lot of investors go wrong. That is the piece we will unpack next, because understanding the mechanics properly is what separates a smart use of negative gearing from a costly guess.

How negative gearing works step by step

Strip away the jargon and negative gearing follows a fairly mechanical process. Every financial year, you tally what your investment property earned, subtract what it cost you to hold, and if the costs win, that shortfall becomes a deduction against your other taxable income. The tricky part is not the concept, it is getting each number right and keeping the paperwork to back it up if the ATO asks questions.

Step 1: Total your rental income

Start with everything the property brought in during the year, mainly rent received, plus any insurance payouts or reimbursements from your property manager. This figure is usually the easy part, since your managing agent’s annual statement lays it out clearly.

Step 2: Add up your deductible expenses

Next, list every cost tied to owning and running the property. This typically includes:

- Loan interest on the investment mortgage (not the principal repayments)

- Council rates, water charges, and land tax

- Property management fees and advertising for tenants

- Repairs, maintenance, and insurance premiums

- Depreciation on the building and eligible fittings, based on a quantity surveyor’s report

Step 3: Work out the net position

Subtract your total expenses from your rental income. If expenses exceed income, you have a net rental loss, and this is where negative gearing actually kicks in.

The loss itself is not the strategy, it is what you do with it against your other income that makes negative gearing worthwhile.

Step 4: Offset the loss against other income

Finally, that net loss gets deducted from your salary, wages, or business income when you lodge your tax return, reducing your overall taxable income and, in turn, the tax you owe for the year.

A worked example of negative gearing in action

Numbers make this easier to grasp than theory ever will. Picture a Melbourne investor earning $95,000 in salary who buys a $650,000 unit with a $520,000 investment loan. The property earns rent, carries costs, and the gap between the two is what actually drives the tax outcome, not the purchase price itself.

The numbers in a typical Melbourne property

Breaking the figures down shows exactly where the net rental loss comes from and how it lines up against the investor’s other income.

| Item | Annual amount |

|---|---|

| Rental income | $24,000 |

| Loan interest | $26,000 |

| Rates, insurance, management fees | $4,500 |

| Depreciation | $3,500 |

| Total expenses | $34,000 |

| Net rental loss | $10,000 |

Once you add up the outgoings against the rent received, the shortfall of $10,000 is the figure that gets carried across to the tax return, not the raw loan repayment or the depreciation schedule on its own.

Turning the loss into a tax refund

Quoting the loss on its own does not save you anything, it is the offset against salary that produces the benefit. That $10,000 loss reduces the investor’s taxable income from $95,000 to $85,000. At a marginal tax rate of 34.5% including the Medicare levy, that translates to roughly $3,450 back at tax time, effectively covering a third of the annual shortfall.

A $10,000 rental loss does not cost you $10,000, it costs you $10,000 minus whatever your marginal tax rate hands back.

Running your own numbers through this same table, using your actual loan balance and rent, tells you far more than any generic rule of thumb ever could.

Risks, alternatives and upcoming rule changes

Negative gearing only works if the maths eventually turns in your favour, and that is where a lot of investors come unstuck. Interest rate rises can widen your annual loss faster than rent increases can close it, and a vacant property for even a few months can wipe out a year’s worth of tax benefit. Treating the strategy as a guaranteed win, rather than a bet on capital growth, is the single biggest risk investors underestimate.

Negative gearing only pays off if the property eventually grows in value enough to cover the losses you have banked along the way.

Common risks worth weighing up

- Cash flow pressure if interest rates rise faster than rent

- Vacancy periods that erase the year’s tax benefit

- Over-reliance on capital growth that may not eventuate in a flat market

- Poor record-keeping, which invites an ATO review of your claimed deductions

Alternatives to consider

Negative gearing is not the only route to building wealth through property. Positive gearing, where rental income exceeds costs, suits investors who prioritise cash flow over tax deductions. Some clients also use SMSF property strategies or diversify into shares and managed funds instead of concentrating everything in one negatively geared asset.

Watching the policy conversation

Negative gearing has been debated in federal politics for years, with various proposals to limit or grandfather the deduction. Nothing has passed into law, but the Australian Government Treasury regularly reviews housing tax settings, so investors should treat the current rules as stable for now, not permanent. Building your strategy with some flexibility baked in protects you if the settings ever shift.

Getting the right advice for your situation

Negative gearing works when the numbers back it up, not just because it is a popular strategy at the pub. You now know how rental losses offset other income, what expenses actually count, and where the risks sit if rates rise or the market stalls. That knowledge puts you ahead of most investors who buy first and calculate later.

Only your own figures, loan balance, rent, and marginal tax rate, can tell you whether this strategy suits your situation. Generic examples get you started, but they will not catch the timing issues or structuring traps that come with business ownership, trusts, or multiple properties. Getting a second set of eyes on your numbers before you commit is worth far more than the interest saved chasing a DIY answer. If you want that clarity before your next purchase or tax return, talk to Gartly Advisory about your property strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}