How to Calculate Capital Gains Tax in Australia

Selling an investment property, a parcel of shares, or a business asset triggers a tax bill most owners don’t see coming. Working out how to calculate capital gains tax in Australia isn’t just plugging a sale price into a formula. You need the right cost base, the correct discount method, and an honest look at your other income for the year, because CGT gets added to your assessable income and taxed at your marginal rate.

This guide walks you through the actual calculation, step by step: establishing your cost base, applying the 50% CGT discount for assets held over 12 months, and using the indexation or ‘other’ method where it applies. You’ll also see how capital losses offset gains, and where SMSF and small business concessions change the numbers entirely.

We’ve run these calculations for hundreds of Melbourne clients over 25+ years, from property investors to trades business owners selling up. Below, you’ll get a practical worked example, the common mistakes that inflate a tax bill unnecessarily, and a clear sense of when the numbers get complicated enough to warrant a proper conversation with an accountant before you sign a contract.

What is capital gains tax and when does it apply?

Capital gains tax (CGT) isn’t actually a separate tax. It’s part of your income tax, triggered by a CGT event, which is usually the sale or disposal of an asset you bought after 20 September 1985. When you sell for more than you paid, the profit gets added to your assessable income for that financial year and taxed at your marginal tax rate. Sell for less than your cost base, and you record a capital loss instead, which you can carry forward to offset future gains.

Most people run into CGT when they sell an investment property, shares outside super, a rental unit, or a business. It also applies to less obvious disposals: transferring an asset into a trust, gifting shares to family, or even losing an asset in a fire and receiving an insurance payout. The ATO treats each of these as a CGT event, even if no cash actually lands in your bank account from a straightforward sale.

If you’ve disposed of an asset in any way, not just sold it, you’ve likely triggered a CGT event worth checking.

Your main residence usually escapes CGT under the home exemption, and assets bought before September 1985 are generally exempt too. But partial exemptions get messy fast, particularly if you’ve rented out part of your home, run a business from it, or lived overseas for part of your ownership period. Superannuation adds another layer: gains inside an SMSF are taxed differently again, often at a flat 15% or 10% concessional rate rather than your personal marginal rate.

Understanding whether a CGT event has actually occurred is the first real decision point. Get that wrong, and every calculation that follows is built on the wrong foundation. The ATO’s guide to capital gains tax is worth bookmarking as a reference point before you start working through the numbers yourself.

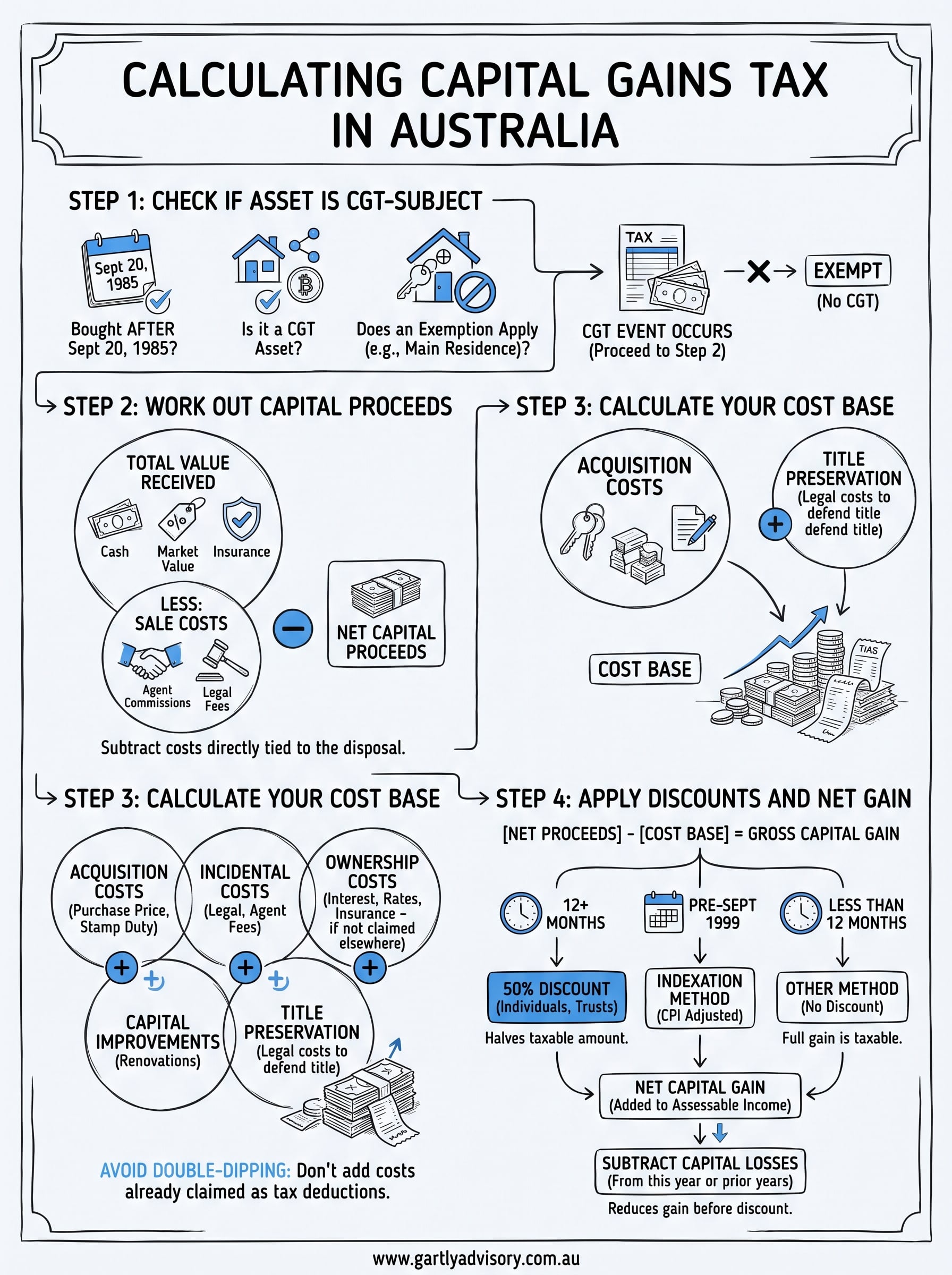

Step 1. Check if your asset is subject to CGT

Before you calculate anything, confirm the asset actually falls under the CGT rules. Start by checking the purchase date. Anything bought before 20 September 1985 is exempt, full stop. Next, work out whether the asset counts as a CGT asset at all: property, shares, units in a trust, business goodwill, and cryptocurrency all qualify. Cars, most personal-use assets under $10,000, and depreciating assets used solely for business (which fall under different rules) generally don’t.

Then check for exemptions. Your main residence is usually CGT-free, unless you’ve used part of it to earn income or rented it out during ownership. Assets held in an SMSF follow separate concessional rates, not your personal marginal rate.

Skip this step and you risk calculating tax on a gain that was never taxable in the first place.

Run through this checklist before moving on:

- Was the asset acquired after 20 September 1985?

- Does it meet the ATO’s definition of a CGT asset?

- Does an exemption apply, such as the main residence exemption?

- Is the asset held personally, in a trust, or inside an SMSF?

Get this wrong and every later step, including your cost base and discount eligibility, is calculated on the wrong asset entirely.

Step 2. Work out your capital proceeds

Capital proceeds are the total value you receive from the CGT event, not just the cash that hits your bank account. For a straightforward property or share sale, this is usually the sale price stated on the contract. But proceeds can also include the market value of anything you received instead of cash, such as shares swapped in a takeover, or an asset transferred as part of a settlement.

Your capital proceeds figure should reflect everything you received in value, not just the deposit and final payment.

Subtract any costs that were part of the sale itself, like agent commissions or legal fees tied directly to the disposal, since these reduce your proceeds before you compare them against your cost base later. Watch for these common adjustments:

- Market substitution rule: if you gifted the asset or sold below market value to a related party, the ATO substitutes market value as your proceeds.

- Earnout arrangements: deferred or contingent payments from a business sale may need separate treatment.

- Insurance payouts: compensation for a lost or destroyed asset counts as capital proceeds too.

Get this figure wrong, particularly on related-party transactions, and the ATO will recalculate it for you, usually with a less favourable outcome.

Step 3. Calculate your cost base

Your cost base is rarely just the purchase price. The ATO recognises five elements: what you paid for the asset, incidental costs like stamp duty and legal fees, ownership costs such as interest and rates (for assets acquired after 20 August 1991), capital improvement costs, and costs of preserving title. Add these together and you often get a much higher figure than the original purchase price alone, which directly shrinks your taxable gain.

Every dollar you can legitimately add to your cost base is a dollar you don’t pay tax on.

Track these components carefully, since missing receipts means missing deductions:

- Acquisition costs: purchase price, stamp duty, conveyancing fees

- Ownership costs: loan interest, council rates, land tax, insurance (only if not already claimed as a tax deduction elsewhere)

- Capital improvements: renovations, extensions, fencing

- Incidental costs: agent fees, valuation fees, advertising for sale

There’s an important rule here: you can’t double-dip. If you’ve already claimed interest or rates as a tax deduction against rental income, you can’t add them to your cost base again. Keep a running spreadsheet from the day you buy the asset, not the day you decide to sell it.

Step 4. Apply discounts and work out your net gain

Once you’ve got proceeds minus cost base, you have your gross capital gain. Now apply the right discount method. Individuals and trusts holding an asset for 12 months or more qualify for the 50% CGT discount, halving the taxable amount before it hits your income tax return. Assets held under 12 months get no discount and the full gain is taxable. Companies never get the discount, though SMSFs in accumulation phase get a third off instead.

Choosing the right method

| Method | Who it suits | Discount |

|---|---|---|

| 50% discount | Individuals, trusts, holding 12+ months | 50% off gain |

| Indexation | Assets bought before 21 September 1999 | CPI-adjusted cost base |

| Other method | Held under 12 months | No discount |

Halving a gain through the 50% discount is often the single biggest lever you have over your final tax bill.

Offsetting losses before you finish

Before calculating tax payable, deduct any capital losses from this year or carried forward from prior years. Losses reduce the gain first, then you apply the discount to what remains, never the other way around. The final figure gets added to your assessable income for the year.

Getting professional help with your CGT calculation

Working through these four steps gives you a solid estimate, but real transactions rarely stay simple. Mixed-use properties, business sales with earnout clauses, and assets held across trusts or SMSFs all pull the calculation in different directions, and a small classification error can cost thousands. If you’ve followed the steps above and the numbers still feel uncertain, that’s the point where a second set of eyes pays for itself.

Gartly Advisory has worked through CGT calculations for property investors, franchise owners, and trades businesses across Melbourne for over 25 years, and we know where the ATO looks closest. Before you sign anything or lodge your return, get the numbers checked properly. Book a consultation with Gartly Advisory and we’ll walk through your specific asset, cost base, and discount eligibility so you pay exactly what you owe, not a dollar more.

{kind=link}

{kind=link}

{kind=link}

{kind=link}