Negative Gearing vs Positive Gearing: Which Strategy Suits You?

Every property investor eventually hits the same fork in the road: do you buy a property that costs you money each month, or one that puts cash back in your pocket? The negative gearing vs positive gearing question sits at the heart of almost every investment property decision we discuss with clients in Ormond and across Melbourne, and getting it wrong can quietly drain your cash flow for years.

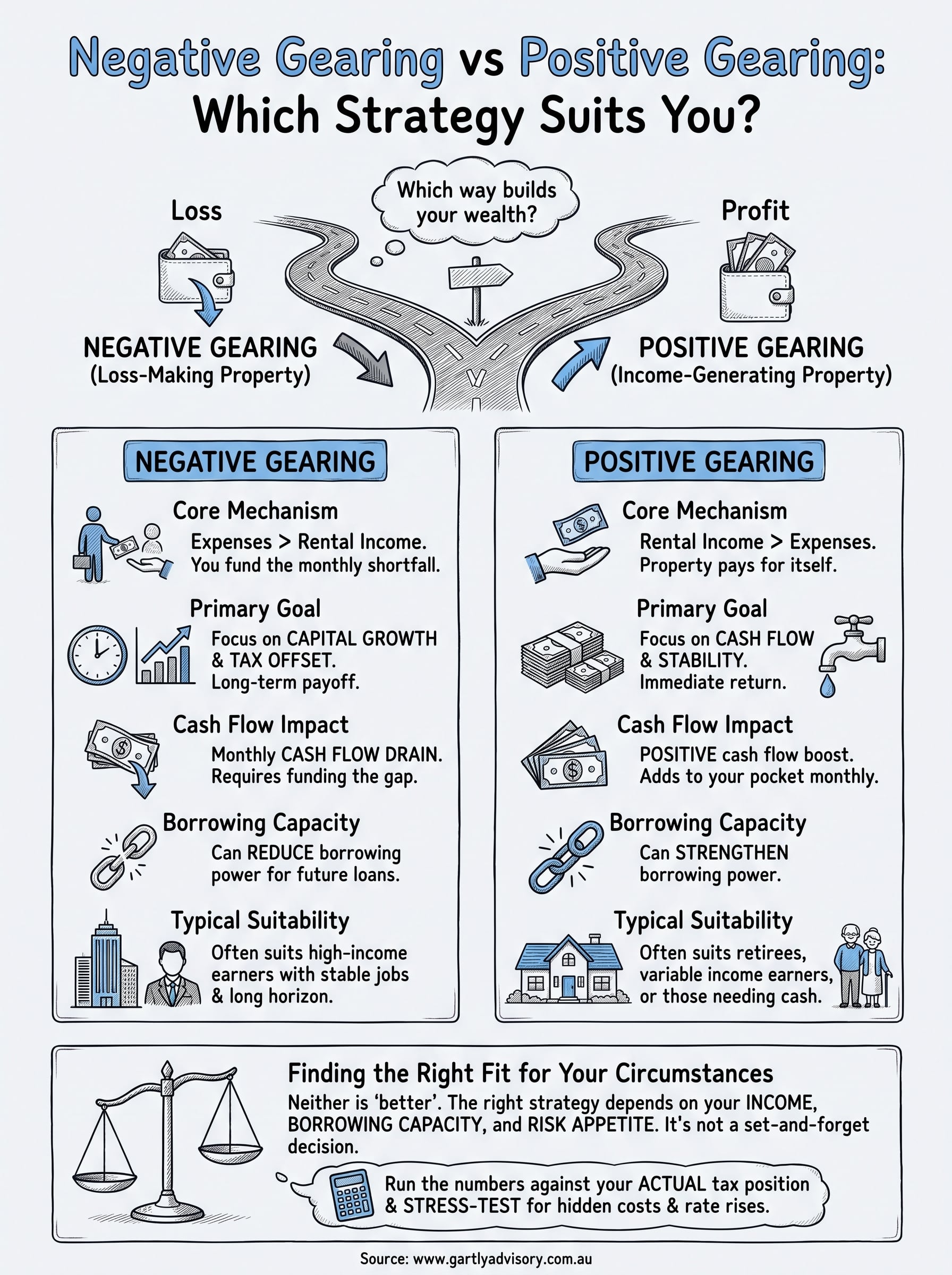

Both strategies are legitimate ways to build wealth through property, but they suit different financial situations, income levels, and goals. Negative gearing works around tax deductions on a loss-making property, while positive gearing relies on rental income exceeding your costs from day one. Neither is automatically better, it depends on your income, borrowing capacity, and what you actually want the property to do for you.

In this article, we’ll break down how each strategy works, weigh up the real pros and cons, and help you work out which approach fits your circumstances. Having advised property investors through three decades of changing tax rules, we’ll also flag the practical traps that catch out even experienced investors.

Why the distinction matters for your investment strategy

Getting your gearing strategy right shapes almost everything about your investment property, from loan structure to how you complete your annual tax return. Choose negatively geared property and you’re planning around losses, using them to offset your other taxable income while banking on capital growth to deliver the real payoff years down the track. Choose positively geared property and you’re planning around income, watching rental returns cover your costs and add to your cash flow from the day the tenant moves in. These aren’t just accounting labels, they determine how much risk you’re carrying and how long you can hold the asset if circumstances change.

The gearing strategy you choose determines whether your property drains your cash flow or feeds it, and that single fact should drive every decision that follows.

Cash flow is where this distinction bites hardest. A negatively geared property might save you tax at the end of the financial year, but you still need to fund the shortfall between rent and expenses every single month. If you lose your job, face an interest rate rise, or hit an unexpected vacancy, that ongoing gap can become genuinely stressful. We’ve seen clients with strong incomes and solid negative gearing setups get caught out simply because they hadn’t stress-tested their monthly cash flow against a rate rise or a few weeks without a tenant.

Borrowing capacity is the other piece lenders scrutinise closely. Positively geared properties actually strengthen your borrowing power because the surplus rental income counts in your favour when a bank assesses your next loan application. Negatively geared properties do the opposite, the shortfall reduces your serviceability, which can limit how many properties you can add to your portfolio. If you’re planning to build a multi-property portfolio, this difference alone can determine how quickly you can grow it.

Finally, your gearing choice interacts directly with your tax position and your income trajectory. High-income earners often lean towards negative gearing because the tax offset is worth more to them, while investors nearing retirement or with lower taxable income often prefer positive gearing’s steady cash return. Neither preference is fixed forever. As your income, super balance, and life stage shift, the strategy that made sense five years ago might not suit you today, which is exactly why this decision deserves more than a one-off conversation with your accountant.

How to work out if your property is negatively or positively geared

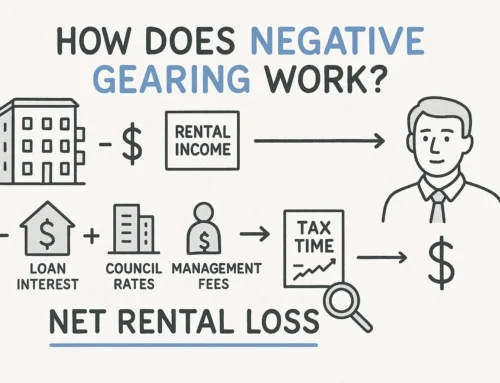

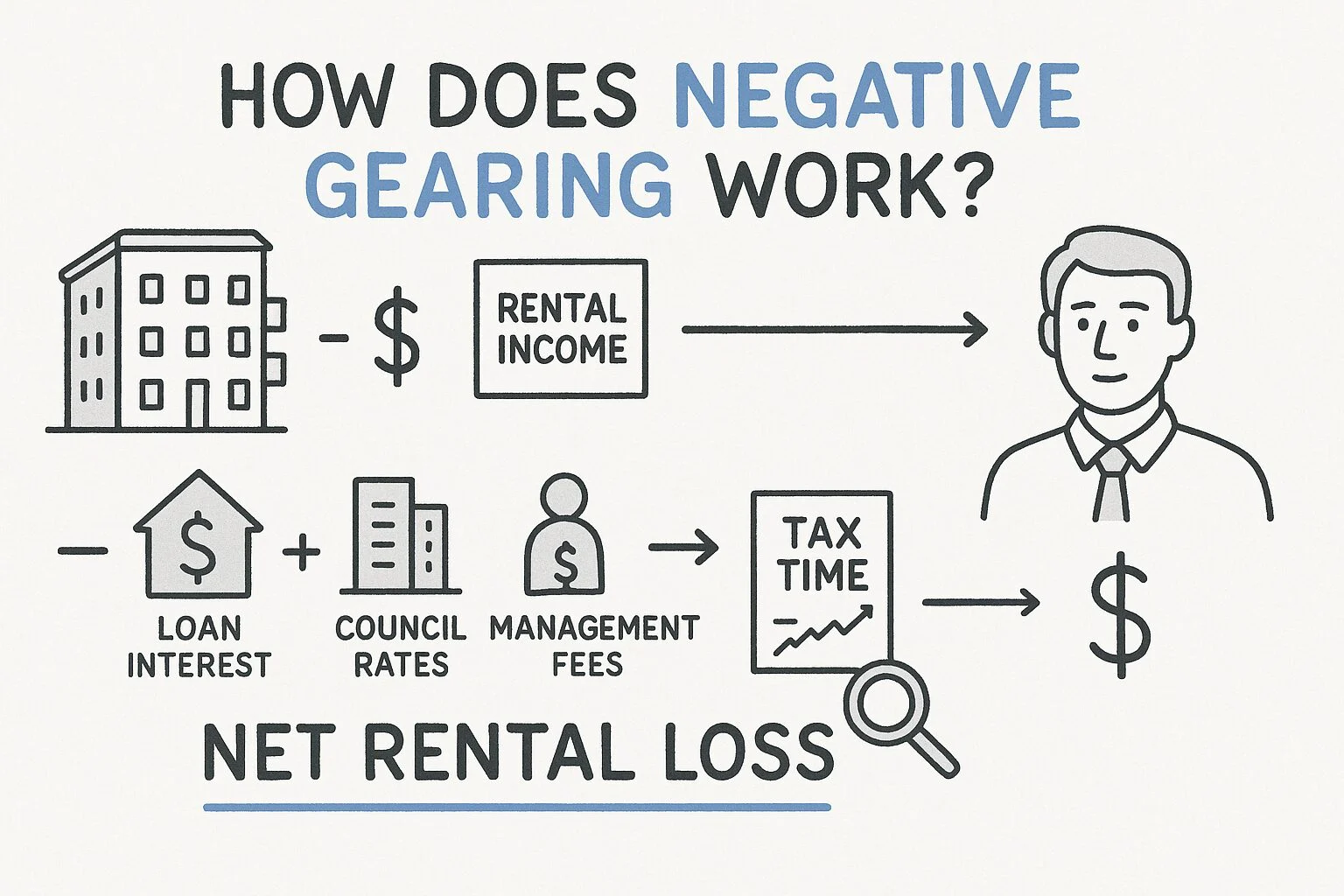

Working out your gearing position isn’t complicated, but it does require pulling together every cost your property generates, not just the mortgage repayment. Rental income minus total property expenses gives you the answer: a negative number means you’re negatively geared, a positive number means you’re positively geared.

The core calculation

Start with your gross annual rent, then subtract everything the property costs you to hold. Lenders and accountants both use a version of this same formula when assessing your position.

Annual rental income

− Loan interest

− Council rates and insurance

− Property management fees

− Repairs and maintenance

− Depreciation (non-cash, but still deductible)

= Net result

If that final number is negative, you’re funding a shortfall every month, no matter how good the tax refund looks in July.

Don’t forget the hidden costs

Budgets often miss the smaller line items that quietly push a property from positive to negative. Landlord insurance, body corporate fees, land tax, and vacancy periods between tenants all belong in the sum. We regularly see investors calculate their gearing position using only the mortgage and rates, then get a shock when quarterly water bills and a month of vacancy blow the numbers out.

Using your loan interest as a single line item also hides risk. A fixed calculation at today’s interest rate can flip from positive to negative gearing the moment rates rise, so it’s worth recalculating with a buffer of at least two percentage points before you commit.

Negative gearing vs positive gearing in practice

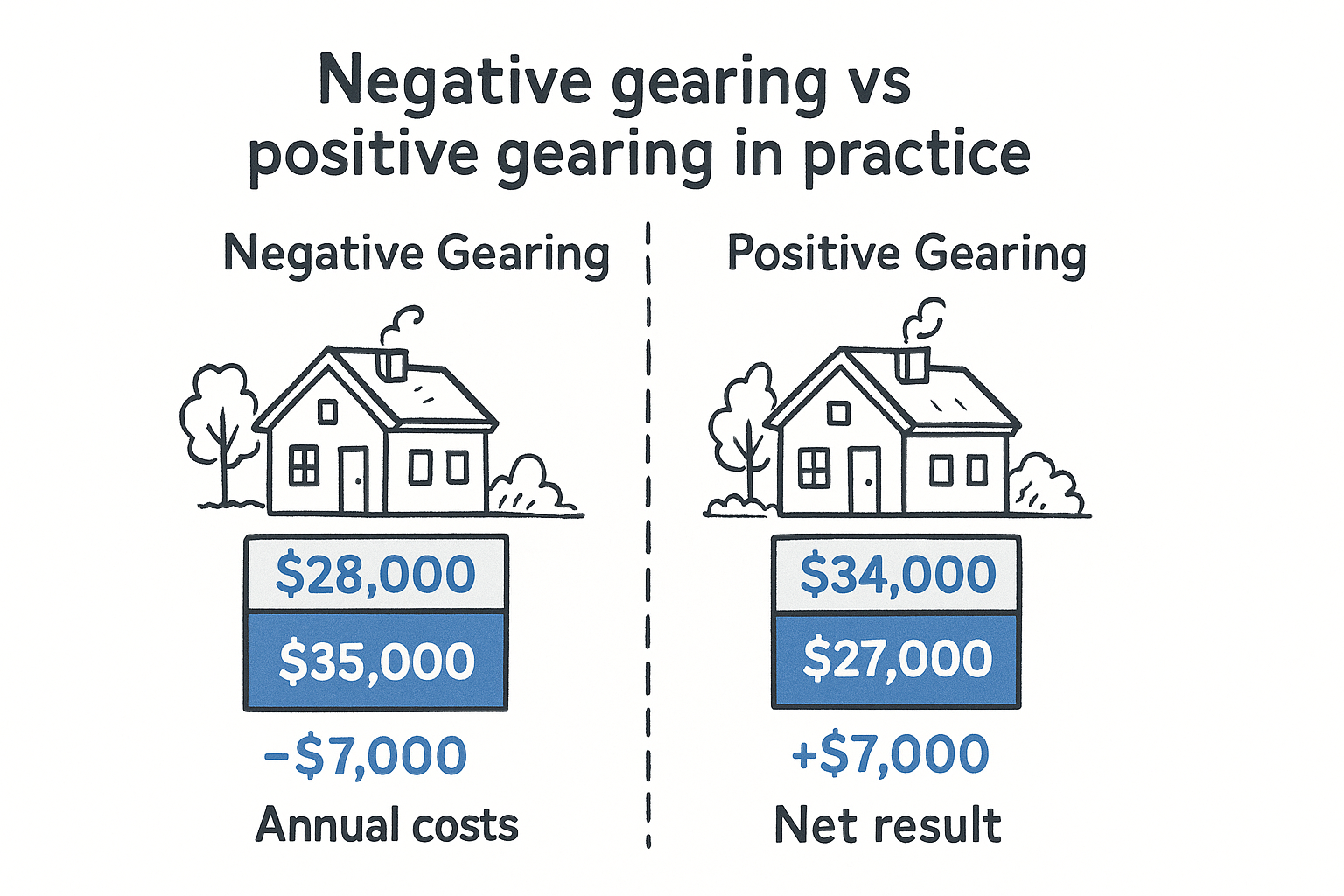

Numbers make this comparison click faster than theory ever does. Take two similar Melbourne properties, both purchased for $650,000, and watch how the cash flow outcome and tax outcome diverge depending on gearing structure.

| Factor | Negatively geared property | Positively geared property |

|---|---|---|

| Annual rent | $28,000 | $34,000 |

| Annual costs (interest, rates, management, repairs) | $35,000 | $27,000 |

| Net result | -$7,000 | +$7,000 |

| Tax impact | Loss offsets other income | Surplus added to taxable income |

| Cash flow effect | You fund the $7,000 shortfall | Property pays you $7,000 |

| Typical location | Inner-city, high growth suburb | Regional or outer-metro, higher yield |

Geoff Gartly often points out that the negatively geared example only works if capital growth actually shows up. If that inner-city property grows 6% a year, the paper loss becomes a rounding error against a $39,000 gain in equity. But if growth stalls, you’ve spent years covering a shortfall for nothing.

Quiet gearing changes trip up investors more than the numbers themselves. A property manager might drop the rent to secure a tenant, or a fixed loan term ending mid-year can push interest costs up overnight. Suddenly a positively geared property is running at a loss, and the owner hasn’t adjusted their budget or their tax planning to match.

Regional markets tend to favour positive gearing because rental yields sit higher relative to purchase price, while capital city inner suburbs skew negative because buyers pay a premium for growth potential rather than yield. Recognising which camp your property sits in from the outset makes planning far easier.

Which strategy suits your goals and risk appetite

Suiting your gearing strategy to your life stage matters more than chasing whatever your neighbour or colleague is doing. Your taxable income, your appetite for monthly cash flow pressure, and how many years you plan to hold the property all point towards one approach over the other.

If growth and tax offset matter most

High-income earners on the top marginal rate often gain the most from negative gearing because every dollar of loss offsets tax at 45 cents rather than 30 or 32.5 cents. This strategy suits people with stable, high income, a long time horizon, and enough buffer to absorb rate rises without stress. It rarely suits someone already stretched thin on serviceability or nearing retirement, when reduced borrowing capacity and ongoing shortfalls become genuine problems rather than tax planning tools.

Choose the strategy that matches your income and risk tolerance today, not the one that worked for someone else five years ago.

If cash flow and stability matter most

Positive gearing suits investors who want the property to pay its own way immediately, including retirees, self-employed business owners with variable income, and anyone uneasy about funding a shortfall every month. Ask yourself these questions before deciding:

- Can I comfortably absorb a two percentage point rate rise without stress?

- Do I need this property to strengthen my borrowing capacity for future purchases?

- Am I relying on capital growth to justify a loss, or do I need income now?

- How many years do I realistically plan to hold this asset?

Your answers usually reveal the right fit faster than any spreadsheet.

Finding the right fit for your circumstances

Neither negative gearing nor positive gearing is the correct answer for every investor. What matters is matching the strategy to your income, your risk tolerance, and how many years you’re prepared to hold the asset. A high-income earner with a long horizon might genuinely benefit from a loss-making property that grows in value, while someone wanting cash flow certainty is usually better served by a property that pays its own way from day one.

Running the numbers properly, including the hidden costs and a realistic interest rate buffer, tells you far more than guessing based on what worked for a friend or colleague. Your circumstances change over time, so this isn’t a decision to set and forget.

If you want someone to run those numbers against your actual tax position and borrowing capacity, talk to Gartly Advisory about which gearing strategy genuinely suits your goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}