Unit Trust vs Discretionary Trust: Key Differences Explained

Choosing between a unit trust vs discretionary trust trips up plenty of business owners, and it’s an easy mistake to make when both structures get lumped together in generic advice online. One splits income and capital according to fixed unit holdings, the other leaves distributions entirely at the trustee’s discretion, and that single difference changes how you’re taxed, how assets are protected, and how easily you can bring in new investors down the track.

If you’re setting up a structure for a family business, a property investment, or a joint venture with unrelated parties, you need to know exactly how beneficiary entitlements work under each option and which one matches your actual goals rather than a generic template. This article breaks down the structural mechanics, the tax treatment, and the practical pros and cons of both trust types side by side.

We’ll walk through how units function like shares, why discretionary trusts suit family asset protection and income splitting, and where each structure falls short. By the end, you’ll have a clear framework for deciding which trust fits your situation, and know when it’s worth getting tailored advice before you sign anything.

Why the trust structure you choose actually matters

Getting this decision wrong doesn’t just create paperwork headaches, it can cost you real money and control over your own business. Unit trust vs discretionary trust isn’t an academic distinction dreamed up by accountants to sound clever. It determines who gets paid, who gets sued, and how easily you can bring in a business partner without triggering capital gains tax or stamp duty on the way. Clients come to us after setting up the wrong structure years earlier, and unwinding it is always more expensive than getting it right from the start.

The cost of picking the wrong structure

Every trust structure locks in a set of rules about how income and capital flow to beneficiaries, and changing those rules later often means resettling the trust, which the ATO can treat as a disposal of assets for capital gains tax purposes. A discretionary trust set up for a family business, then converted to a unit trust to bring in an external investor, can trigger exactly this problem. Consider the practical fallout of getting the structure wrong from day one:

- Unexpected CGT or stamp duty bills when restructuring

- Disputes between beneficiaries over who was entitled to distributions

- Asset protection gaps that expose personal wealth to business creditors

- Difficulty attracting investors who want clearly defined, fixed entitlements

- Extra accounting fees every year just to manage an ill-fitting structure

The trust structure you choose on day one shapes your tax bill, your asset protection, and your options for years afterwards.

Asset protection and control differ sharply

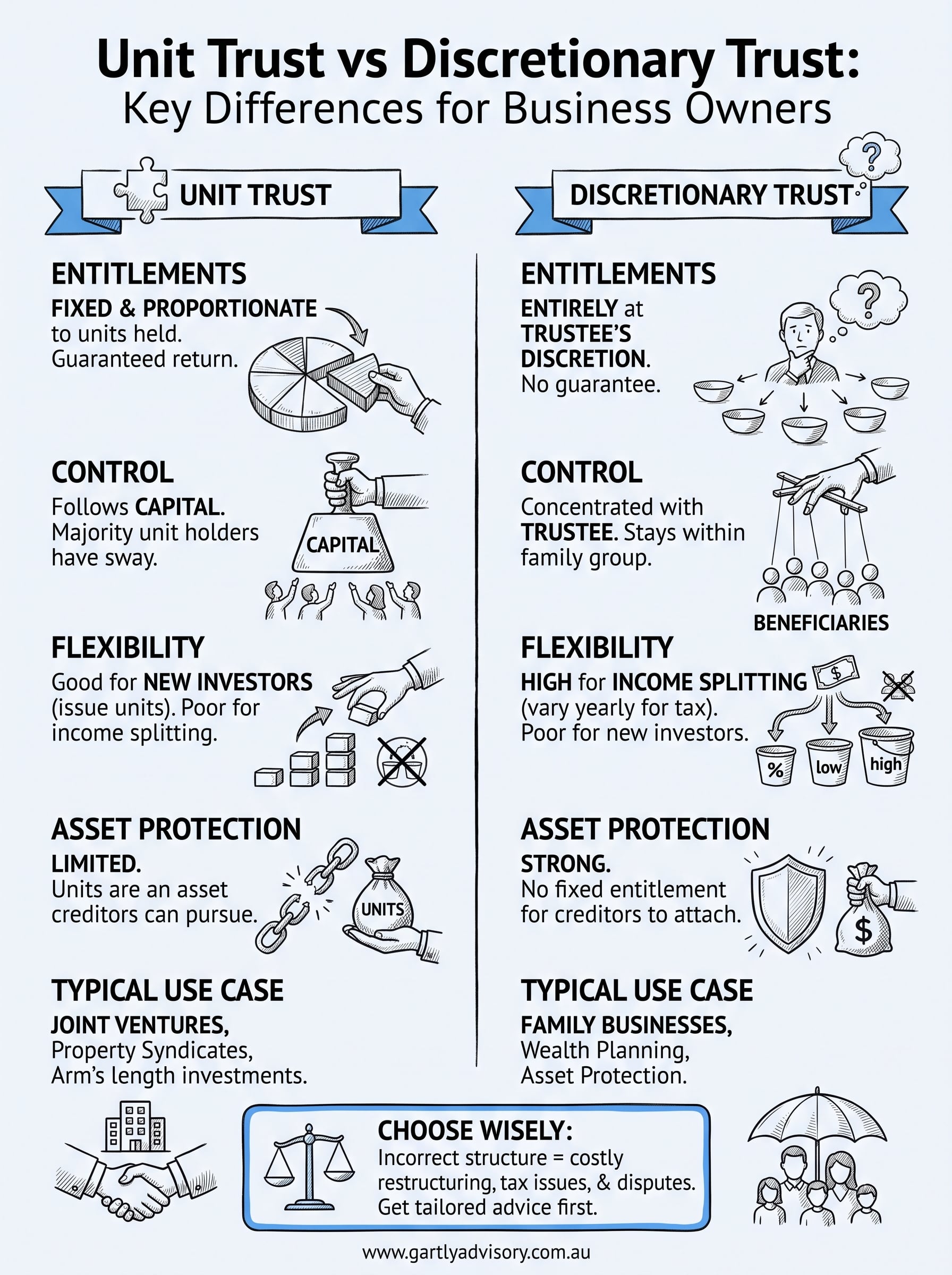

Discretionary trusts give the trustee full discretionary power over who receives income and capital each year, which is exactly why they’re popular for family businesses wanting flexibility and a layer of protection against creditors chasing an individual beneficiary. Nobody has a fixed entitlement until the trustee actually makes a distribution, so a beneficiary’s personal creditors generally can’t force a claim against trust assets. Unit trusts work differently. Each unit holder owns a defined, proportionate interest, much like a shareholder in a company, and that fixed entitlement means creditors of a unit holder can potentially pursue those units directly. If asset protection is your main concern, that distinction alone can settle the decision.

Bringing in new investors or partners

Joint ventures and arm’s length investment arrangements almost always favour unit trusts, because investors want to know precisely what percentage of income and capital they’re entitled to before they commit any money. Nobody putting real capital into a project wants their return sitting entirely at someone else’s discretion. A discretionary trust, by contrast, works well when everyone involved is family, and flexibility to split income between spouses, adult children, or a corporate beneficiary matters more than fixed certainty. We regularly see hybrid trusts used where a business needs both features, though that adds complexity that needs proper legal and tax advice to manage correctly, so it’s not a decision to make from a template found online.

Getting professional guidance early, before assets are transferred or investors sign on, avoids the costly restructuring problems outlined above. The Australian Taxation Office publishes guidance on how trust structures are taxed, and it’s worth reading before you commit to either structure, though nothing replaces advice tailored to your actual business and family circumstances.

How to decide between a unit trust and a discretionary trust

Picking between a unit trust vs discretionary trust comes down to answering a handful of practical questions about who’s involved, what you’re protecting, and how much flexibility you actually need. Skip the theory for a moment and think about your own situation: are you running this with family, or with people who expect a defined return on their money? That single question eliminates half the guesswork straight away.

Questions to ask before you commit

Run through these before you talk to your accountant, so the conversation starts with your goals rather than a blank slate:

- Are the beneficiaries all family members, or does the group include unrelated investors or business partners?

- Do you need to split income each year based on tax position, or do participants expect a fixed, proportionate share?

- Is asset protection from creditors a bigger priority than certainty of entitlement?

- Will you need to bring in new capital or new unit holders in the next few years?

- Are you running an operating business, holding property, or pooling investment funds?

Matching the structure to your goals

Family businesses wanting income-splitting flexibility and a protective barrier around personal assets almost always land on a discretionary trust. It suits situations where distributions change year to year depending on who’s studying, who’s on a lower income, or who needs support that year. Joint ventures, arm’s length property investments, and situations with external capital lean towards a unit trust, because everyone involved wants their entitlement fixed and transparent from day one, not subject to someone else’s annual decision.

If your beneficiaries are family, flexibility usually wins; if they’re investors, certainty usually wins.

When a hybrid structure makes sense

Some businesses genuinely need both fixed entitlements for outside investors and discretionary flexibility for the family group running the operation. A hybrid trust combines unit and discretionary elements, giving investors defined units while letting the trustee retain discretion over a separate pool of income or capital. This isn’t a structure to build from a generic template, because the drafting has to correctly separate the fixed and discretionary components or you risk losing the tax and asset protection benefits of both. Talk to an adviser who has actually drafted these deeds before, not just read about them.

Whatever you decide, get the paperwork right before money changes hands or assets move into the trust. Restructuring later, as covered above, almost always costs more than getting proper advice upfront.

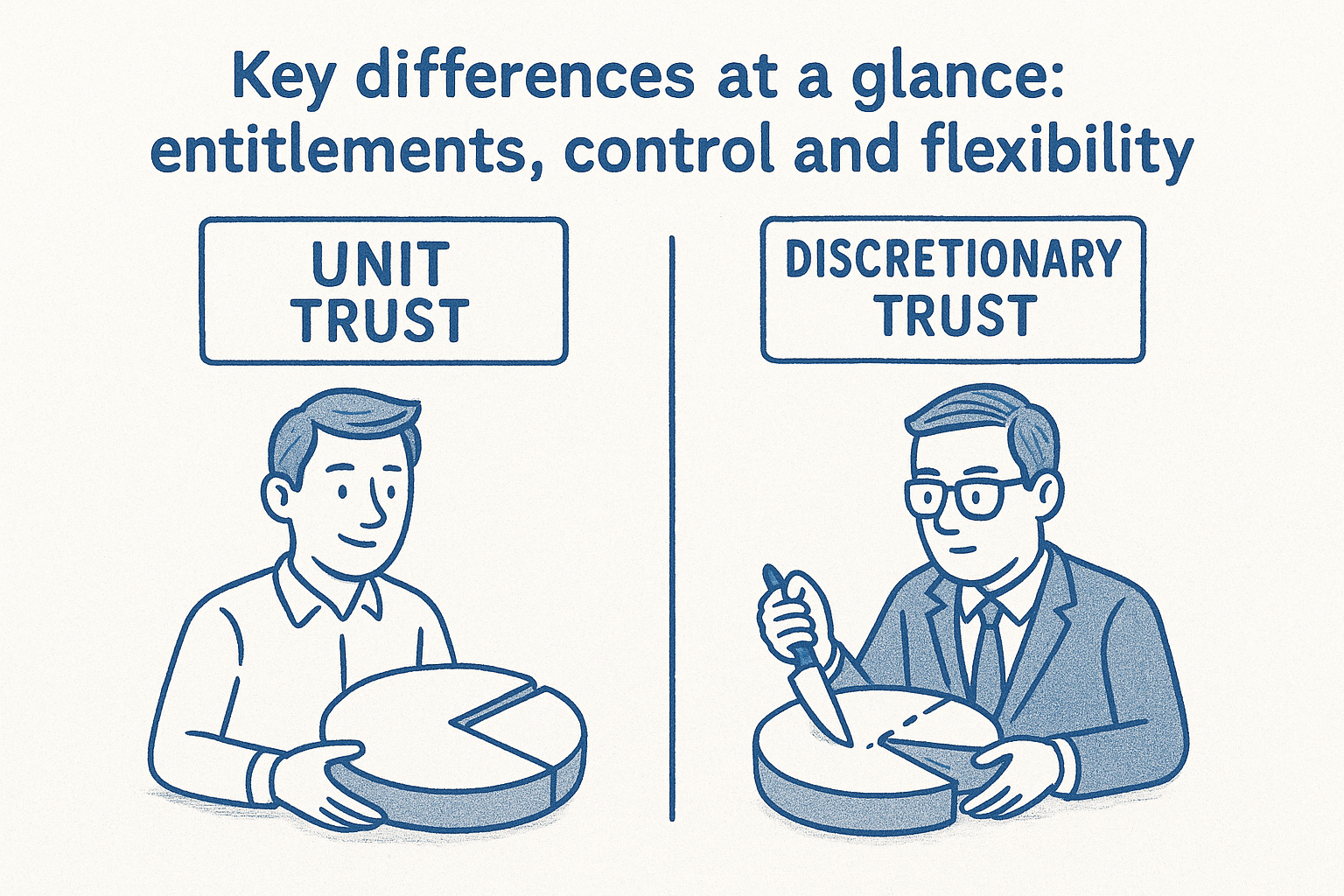

Key differences at a glance: entitlements, control and flexibility

Side by side, a unit trust vs discretionary trust looks less like two flavours of the same product and more like two different legal animals wearing the same trust label. One gives every holder a fixed, tradeable slice of the pie; the other gives the trustee a free hand to slice it however suits the family that year. The table below sets out the practical differences you’ll actually run into.

| Feature | Unit Trust | Discretionary Trust |

|---|---|---|

| Beneficiary entitlement | Fixed, proportionate to units held | Entirely at trustee’s discretion |

| Income splitting | Not possible, fixed by unit holding | Highly flexible, can vary yearly |

| Asset protection | Limited, units are an asset creditors can pursue | Strong, no fixed entitlement to attach |

| Bringing in new investors | Straightforward, issue new units | Difficult, requires trust deed changes |

| Typical use case | Joint ventures, property syndicates | Family businesses, wealth planning |

Entitlements decide who gets paid

A unit holder owns a defined percentage of the trust, so distributions follow that percentage automatically, regardless of anyone’s personal tax position that year. A discretionary beneficiary has no such guarantee. They might receive a large distribution one year and nothing the next, purely because the trustee decided it made better tax or commercial sense.

Fixed units guarantee a return; discretionary status guarantees nothing until the trustee signs off.

Control sits with different people

In a unit trust, control genuinely follows capital, much like shareholding in a company, so a majority unit holder has real sway over decisions. A discretionary trust concentrates control with the trustee, who can be a company directed by family members, meaning day-to-day decision-making stays inside the family group even as beneficiaries change.

Flexibility works in opposite directions

Unit trusts flex well when you need to bring in fresh capital or new partners, because issuing units is administratively simple compared to rewriting a discretionary deed. Discretionary trusts flex well on the income side instead, letting you shift distributions to whoever has the lowest marginal tax rate that year. Neither structure gives you both kinds of flexibility at once, which is exactly why the choice matters so much before you commit.

Tax, compliance and practical setup considerations

Tax treatment separates these two structures almost as sharply as control does. Discretionary trusts let the trustee stream different categories of income to different beneficiaries, taking advantage of individual tax-free thresholds and lower marginal rates, but a missed family trust election can trigger family trust distribution tax on amounts paid outside the family group. Unit trusts, on the other hand, generally can’t split income by category, and unit holders pay tax on their proportionate share whether or not cash actually landed in their account that year, which catches out first-time investors expecting distributions to match profit exactly.

Setting up either structure properly starts with a properly drafted trust deed, not a downloaded template. Registering for an ABN and TFN, opening a dedicated trust bank account, and appointing a corporate trustee through ASIC where appropriate all need to happen before any money moves. Skipping these steps, or getting the deed wording wrong, is exactly what creates the expensive restructuring problems covered earlier in this article.

Get the deed and registrations right at setup, because fixing them later almost always costs more than doing it properly the first time.

Ongoing compliance obligations

Both structures carry genuine annual paperwork, and missing a step can undo the tax benefit you set the trust up to capture. Discretionary trusts need signed distribution resolutions before 30 June each year, or the ATO can tax undistributed income at the top marginal rate. Unit trusts need accurate unit registers and consistent record-keeping of capital calls and redemptions, since unit holders rely on those records to justify their reported share of income.

Checklist for annual compliance, regardless of which structure you run:

- Lodge the trust’s annual tax return by the due date

- Prepare and sign distribution resolutions or unit distribution statements before year-end

- Keep the unit register or beneficiary schedule current

- Reconcile trust bank accounts against the trust’s financial statements

- Review the trust deed periodically against current tax law

Compliance work is also where an experienced adviser earns their fee. Getting the ATO’s trust registration and reporting requirements wrong, or missing a resolution deadline, can wipe out the tax advantage either structure was meant to deliver.

Finding the right structure for your situation

Weighing up unit trust vs discretionary trust always comes back to who’s involved and what you’re protecting. Family businesses wanting flexibility and asset protection generally suit a discretionary trust. Joint ventures and investors wanting fixed, transparent entitlements suit a unit trust. Neither choice is automatically right, and picking the wrong one can lock you into costly restructuring down the track, exactly the outcome you’re trying to avoid.

Templates and generic guides only get you so far. Your family circumstances, growth plans, and appetite for outside investment all shape which structure actually works, and getting the trust deed wrong at setup is far more expensive to fix than to prevent. Talk it through with someone who’s drafted these deeds before, not just read about them.

If you’re weighing up which structure suits your business or investment goals, book a consultation with Gartly Advisory and get advice tailored to your actual situation before you sign anything.

{kind=link}

{kind=link}

{kind=link}

{kind=link}